After writing a blog post on why India needs long-term FDI – in addition to boosting international trade – I began thinking of how globalisation might have adversely impacted this particular kind of flow of foreign capital in recent decades. It has become the fashion of recent years for western advanced economies to express their discontent with globalisation because of the loss of jobs and livelihoods there. While globalisation has largely been praised as a force for good in developing economies around the world, and I have myself written about the millions of new jobs and skills it has created in developing and emerging economies around the world.

However, this rather simplistic way of looking at globalization of business misses an important point and it is that in diversifying their manufacturing operations around the world, MNCs (multinational corporations) didn’t necessarily always invest in building technological capabilities in the host countries. They merely treated them as manufacturing locations that offered them huge benefits through labour cost arbitrage and transfer of technology wasn’t part of the investment deal anymore. It used to be true of most foreign direct investment in India at one time, especially in industrial goods and even automobiles, that the foreign company would enter into a technical and financial collaboration with the Indian partner company and this meant joint collaboration on production, transferring their technology to the Indian company over time. This helped Indian businesses immensely in gaining access to new technologies, increasing their own knowledge, capabilities and skills.

Perhaps we are underestimating the importance of this kind of FDI in today’s globalized world of business. I think some of it might have been due to the fact that this wave of globalization that began in the mid-1990s was led by financial companies and flows that spread throughout the world, causing the link between technical and financial collaborations to break. Governments of developing and emerging economies were also only too happy to welcome foreign investment into their countries, in the widespread economic liberalization that was taking place. This was mostly in low to medium skill and value-add industries in manufacturing, since many of the developing and emerging economies were not equipped with a highly educated, skilled and trained workforce required for higher-technology and high-value add industries. And finally, the fact that many countries’ governments removed caps on foreign direct investment in a variety of industries meant that MNCs could set up wholly owned subsidiaries in the host countries and take advantage of low labour costs.

In large economies such as India and China, or even Brazil, you could say that they might have been there for the domestic market as well, but in most other countries, this was not the main deciding factor. MNCs set up manufacturing operations in several countries with a view to lower costs of production and are able to export these anywhere else in the world, and have little to no long-term commitment to the country they are investing in. They retain their intellectual property, their technology, and earn royalties, etc which are repatriated to their home countries, along with substantial profits.

In the process, I believe many developing and emerging economies are giving up on building their technological capabilities and therefore, on their economic future. In addition, the kind of manufacturing that companies engage in has itself changed dramatically over the past three decades. From trying to save on inventory costs and therefore adopting what was called just-in-time manufacturing, to the complex global value and supply chains we have today, manufacturing has itself become so atomized that countries are now producers of components and parts, or are assemblers of finished products.

Between these, it is clear that it is in the making of components, parts and intermediate goods that the greater value lies, because it is more upstream, it incorporates intellectual property and it creates a competitive advantage for the MNC or the country. However, this is still not the core competence that CK Prahlad and Gary Hamel had written about decades ago, because manufacturing has become much too fragmented and atomized for it. That core competence concept mainly came from Japanese companies and others in East Asia, where they could take a particular part or aspect of manufacturing and innovate hugely in making it even better, until the company came to dominate that particular area. For example, you could say this of Samsung even today in memory chips and display screens, and of many Japanese companies in the area of imaging technologies and opticals. Some of it is also true of German mittelstand companies that make highly specialized machinery and equipment parts and components.

The other aspect to consider is that manufacturing and all of industry has been disrupted by information and digital technology in this century in what is being called Industry 4.0. In this age of Industry 4.0 and of global value chains or GVCs as they are called, how can developing and emerging economies grow their technological capabilities through foreign direct investment?

Many developing and low-income countries begin as assemblers of finished products for MNCs and then work their way into specialized areas of manufacturing. However, this needn’t always be the case, as the phenomenon of contract manufacturing catches on. If we recall, the manufacturing and assembly of Apple iPhones in China for example, especially by Taiwanese companies such as Foxconn and Hon Hai were the first to shift out of China when the US raised tariffs on China in Trump’s first term. This proves how mobile and unrooted this type of manufacturing can be; in fact, today, India is manufacturing more Apple iPhones than China thanks again to companies engaged in contract manufacturing, including a Tata company. China has since moved on, to much more high-tech manufacturing and innovations of their own, as is evident from their overcapacity in advanced and high-tech industries from EVs and electric battery technology to solar energy and AI.

On reading a 2015 policy paper from the OECD on the participation of developing countries in GVCs, I was struck by how much developing countries’ GVC participation revolves around the production of, and trade in, intermediate products. And it is almost entirely related with trade, not so much with FDI and long-term investment. This is the crux of the matter I am writing about in this blog post. Further, the fact that between Africa and Asia (the two continents taken for purposes of the OECD paper) Asia, particularly South-east Asia dominates in GVC related to high-tech consumer products and automobiles, while in Africa, the authors report that the “idea of a factory Africa” has yet to be born, with most of the GVCs in agricultural goods, minerals and extractive industries.

This OECD policy paper does not include Latin America at all, but I would imagine that many Latin American economies such as Brazil, Argentina and Chile would be in a state of industrialization somewhere between Africa and Southeast Asia/East Asia, in the sense that they have a stronger industrial base than many countries in Africa. That said, most Latin American economies still rely on agricultural products and other commodities as exports to the developed world. This must change, of course. In an old blog post of mine, I had attempted a SWOT analysis of economies/economic regions around the world and had suggested ways in which they could minimize their weaknesses and threats. Almost five years later, most of my analysis would hold true even today.

In the context of Industry 4.0 which the developed world is fast moving towards and so are many emerging and developing economies, we must consider what effect this extent of atomization of manufacturing and GVCs are likely to have. I can think of a few broad features of this kind of new economy as I have already written about on my blog. These are

- Industry and economy driven by digital technology

- Complex global value and supply chains

- Greater servicification of the economy

- Cleaner technology with less dependence on fossil fuels

Against this kind of industrial future, what chance does wider sharing of technology between the developed and developing world have? And instead of fragmenting manufacturing itself to tiny components sourced from many countries, shouldn’t we be thinking of a global value chain that is based on sub-assemblies, wherein it is at least possible for companies to innovate more, develop more specialized core competencies and gain competitive advantage, while also allowing the underlying technology to diffuse more widely throughout the economy? It is for companies, including MNCs to think long and hard about this and find a better way forward.

And what about governments playing a more important and responsible role in framing policies that invite foreign investment in industry and manufacturing on the condition that local companies and the wider economy benefits from technology transfer. In opening up the economy to 100% FDI through the automatic route, as we do in India for many industries, we must not forget the need for the host country to gain from new technological capabilities and wider technology diffusion. This is something that China has done very successfully through most of its economic liberalization programme, and now that it has developed those technological capabilities it can go it alone as it decided to do with the China Industry 2025 programme launched in 2015. It appears that Vietnam has also followed a similar FDI policy with sectoral caps and the need to partner with a local firm.

Wider diffusion of technology also allows developing and emerging economies to advance their innovations and register patents, including those jointly developed with a foreign country partner firm. Here, I must mention once again the need to revisit patent laws in order to encourage innovation on an economy-wide scale.

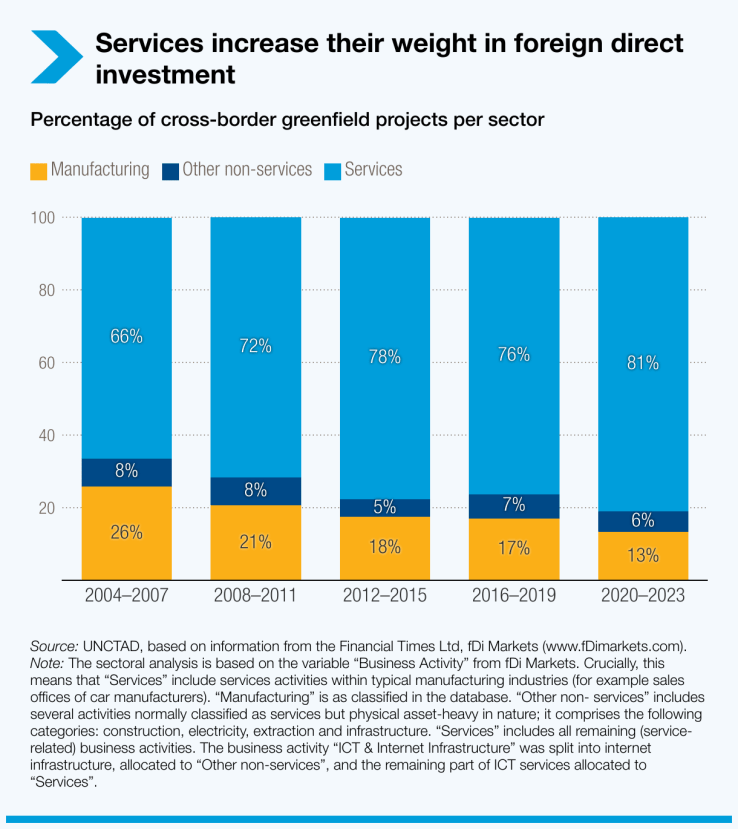

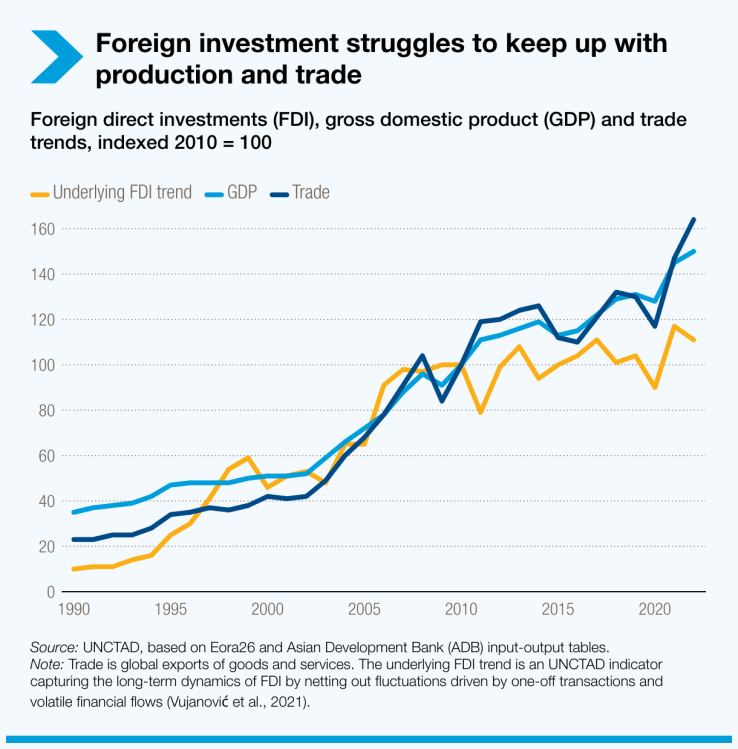

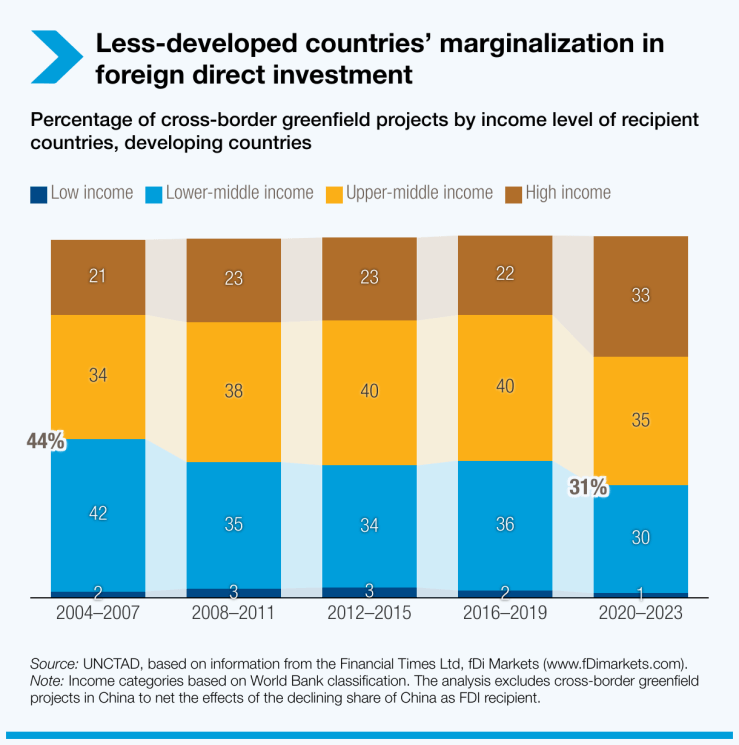

In recent years, unfortunately, FDI has also tended to be concentrated in developed economies and in capital intensive industries such as financial services and in data centres, according to UNCTAD. This might even be shifting capital away from clean energy transition and renewables which is not a good development. Also, in recent years, it has been foreign trade that has dominated the entire economic landscape, rather than long-term foreign investment and even domestic private investment. What’s more, increasingly it is bilateral trade agreements and FTAs that are favoured over and above anything else. This not only undermines the WTO trading system, it is pursuing short-term growth by reaching for low-hanging fruit. The harder, longer-term path to economic growth lies through building capacity, and it comes from investment in R&D, innovations, and in creating new and better-quality jobs for millions around the world.

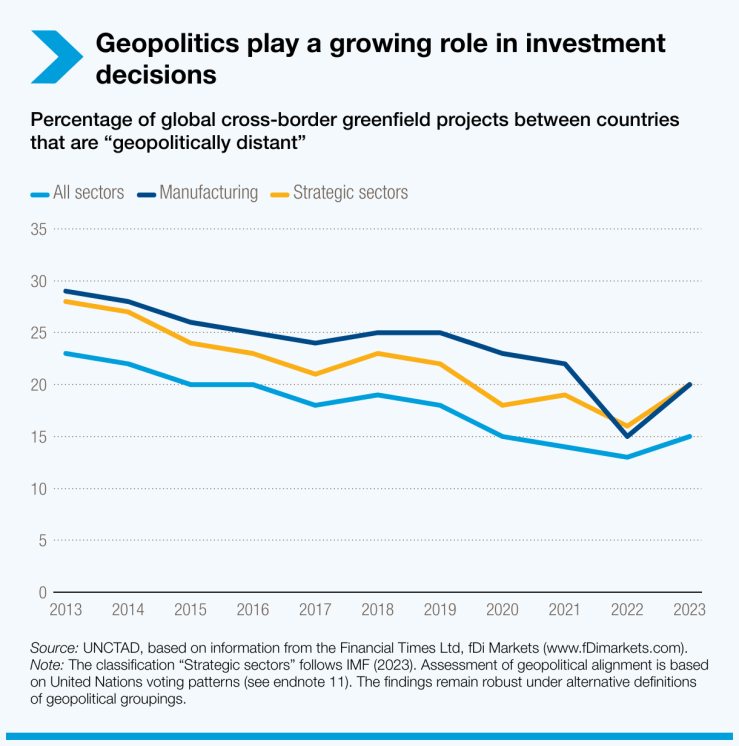

Today, it is also geopolitics that decides the direction and nature of investments around the world, which I had written about in a blog post about offshoring. With the result that not only is the last wave of globalization being reversed and upended, it is being taken in directions not beneficial to the developing and poorer world. Time for governments and businesses in the Global South to assert their need for long-term FDI and to build their technological capabilities so that they are not left behind economically.

The featured image at the start of this post is by Steve Johnson on Unsplash