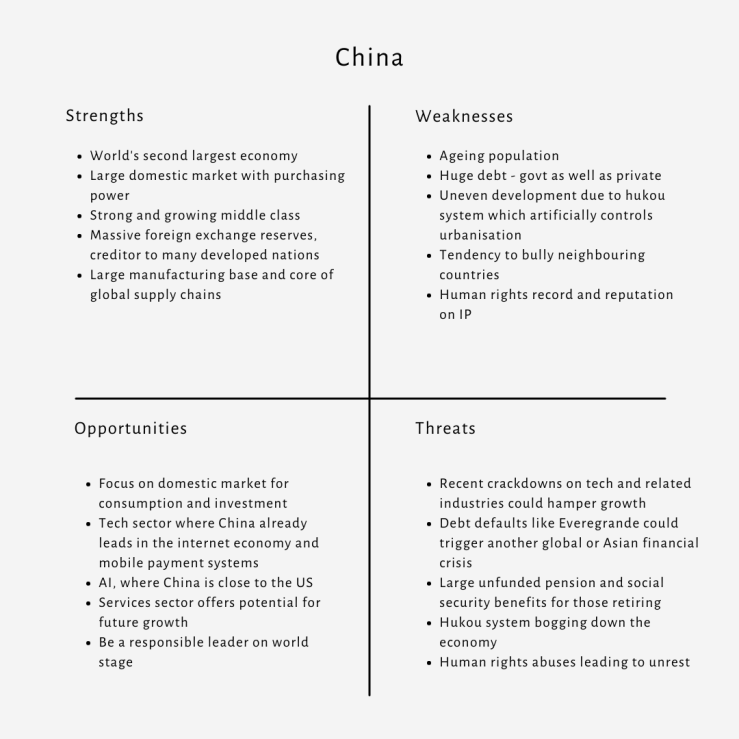

As countries report their September 2021 quarter GDP growth rates, the world will be eagerly watching to read and parse the news and data. So far, China has reported a much lower than expected GDP growth at 4.9% over the previous year. I am not sure how much of that is due to the government’s crackdown on various parts of the tech sector, because I think those will still take a few quarters to play out. Consumption is believed to have been strong, while fixed asset investment has been muted due to controls on credit to certain industries. The steel sector in China, for example, has been forcibly shrunk to comply with the country’s commitment to the targets for carbon emissions reduction.

However, it is not very encouraging news for the global economy. As I have written before, China’s economy has a huge impact on the global economy, most of which is felt through global trade and investment flows. And while China might be on an indigenization programme as part of its China 2025 strategy, and while the rest of the world too tries to reduce its dependence on China, it is still a big market for most goods and services. The other impact on the global economy which is linked to the first one is commodity prices. This too has spiked, ever since China first recovered from the Covid pandemic last year.

While we wait for the Western economies as well as India and large emerging economies to report their economic growth for the September quarter, we must keep in mind that most of the growth will be due to a base effect since the same quarter last year was one of near-total lockdowns. The growth that we are likely to see in Western economies would be mostly on account of consumption coming back thanks to generous relief and stimulus measures to households as well as businesses.

In India, the growth would still be largely due to some private consumption as well as government investment. Private sector investment would still be muted in India, because consumption and investment demand are still low and have been weak for a long time, prior to the pandemic. And there wasn’t much by way of relief to the poorer and economically weaker sections in India, even as the second wave of the pandemic raged earlier this year.

Large sections of the service sector across all economies are still battered and even if they are reopening in some areas, their contribution to economic activity is likely to be weak. The increase in pent-up demand has caused unprecedented shortages of many products and commodities, not least of which is energy. This, because much of the Western world as well as China are trying to shift to a less fossil fuel dependent economy, thanks to the climate change imperative.

It appears, therefore, as though all three challenges are coming together at a terrible time: dealing with the pandemic and climate-related challenges when consumer demand and economic activity are beginning to see a revival. Balancing the needs of all three and planning a smooth recovery path without choking off growth is going to prove challenging.

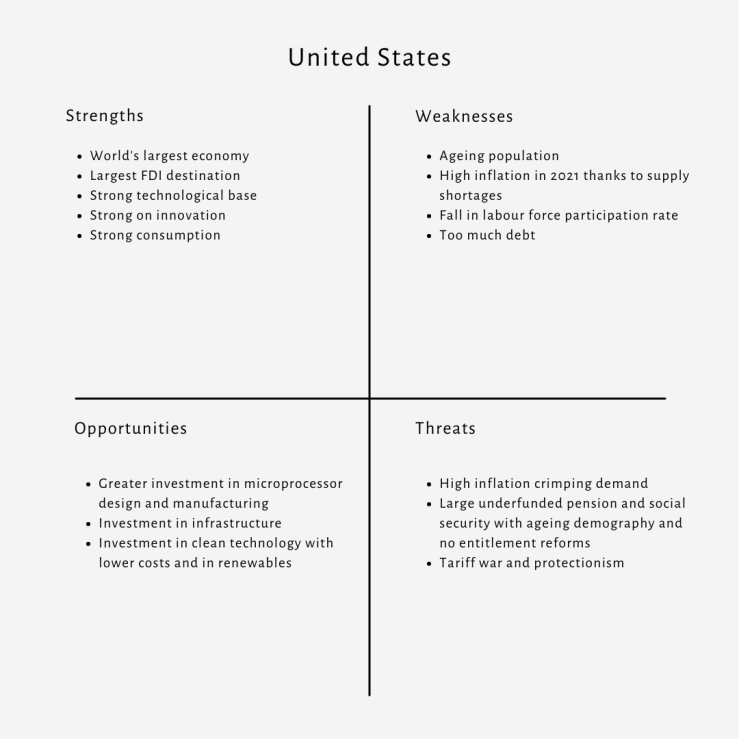

Besides, we also have other threats looming on the horizon. Higher inflation which, if it sustains, will start to hurt growth. Then, there are the huge fiscal deficits and debt that most countries have piled up, thanks to the spending that was required by governments to control the pandemic. And there are regional peculiarities such as south-east Asian economies hurt by successive waves of Covid, mostly due to the Delta variant, the shortages of workers in several industries in the West even when there are jobs available, and economies in Latin America as well as Africa that are still battered by Covid.

If we take just inflation itself, it takes a very different form in Western economies where wages have been rising steadily and many places have also initiated a minimum wage increase during the pandemic to boost incomes and spending. And because there are still unfilled job vacancies, there is likely to be further upward pressure on wages. Then, there is the part that is linked to supply shortages, of course, which is hopefully only transitory.

However, in India and in other emerging economies the inflation we are experiencing is of the cost-push kind thanks to the spike in prices of commodities and inputs. In India, this kind of inflation is particularly exacerbated by the central government’s decision for many years to impose high excise duties and taxes on fuel, not realizing the effect it can have on inflation across the board and as a consequence, on crimping consumer demand.

In fact, this has the potential to stall economic growth in India, given how fossil-fuel dependent we are as an economy. It can certainly stall growth in the automobile sector, which only recently experienced some growth after several years of weak demand. It has been reported that high prices of fuel are pushing Indian consumers to consider electric cars. And while on the face of it, that might appear a positive development, it is anything but. Precisely because our source of energy even for electricity is coal. Speaking of which, coal shortages are already plaguing the country, since the Indian government appears to have failed to anticipate coal requirements, with the spurt in economic activity.

On the ballooning fiscal deficits and debt levels across the world, particularly in Western economies, there is not much that can be done to contain fiscal deficits, since governments had to intervene in job protection and economic relief. The amount of monetary stimulus can certainly be tapered gradually, since most of it is only boosting all investment asset classes, especially stock markets, and the US Federal Reserve has already hinted that it might start drawing down the monetary stimulus, November 2021 onwards. It also looks like it might have to start raising interest rates next year itself if high inflation were to persist, and not in 2023, as suggested earlier.

The problem is with low-and-middle-income countries that have taken on huge amounts of debt. They need to have a clear plan for how they can lower it in the coming months and years, and multilateral institutions as well as global investors need to show greater forbearance.

In India too, we have seen our fiscal deficits spike to unprecedented levels in recent times (9.3% for FY21 and 6.8% target for FY22), but here again, the government had to take the decision to borrow and spend, while still planning for sustainable debt-reduction. Strangely enough, tax revenues have been buoyant though whether that is sustainable is not clear. Besides, a large part of the tax collection in India are indirect taxes, of which just those on fuel, are eye-watering. We have also seen monthly GST tax collections go back to almost pre-pandemic levels, but that could also be because of higher prices across the board and not necessarily because of greater economic activity.

On weak demand in India and emerging economies, it is dependent on employment and well-paying jobs. Unemployment in India is lower in the past couple of months according to CMIE, but with most service sector industries still down, private sector hiring is not that high. Also, most jobs in India were lost in small and medium scale enterprises at the start of the pandemic and during the second wave, and those are the biggest job creators in the economy. Fiscal relief to the poor and economically vulnerable population was almost negligible this year, even with the second wave of Covid-19, except for an extension of free foodgrain distribution through PDS (Public Distribution System). I suppose, as I said in an earlier piece, the big relief package might still be round the corner – just ahead of assembly elections in many states next year. I hope they are not waiting for the third wave to happen before then!

It appears, therefore, that the world is still not out of the woods. Just as a thought experiment, I have attempted a SWOT analysis of what the different economic regions of the world might be experiencing and what their biggest threats could be, as well as opportunities that lie ahead. While these might seem a little simplistic at the moment, they do indicate some broad-brush priorities and requirements in a big-picture view.

The economies of the South (from Latin America in the west to Africa and South Asia) all need to invest much more in education, skills upgradation and in technology. They also have opportunities to shift from commodity exports to contract manufacturing as the next step.

South-east Asia and East Asia seem to have been the bright spots in the global economy for the past couple of decades, leading the world in consumer electronics and microprocessors, among other high-tech manufacturing. In fact, the world is experiencing a massive chip shortage precisely because those economies control global chip manufacture, and most of them have been in extended lockdowns thanks to new waves of Covid this year.

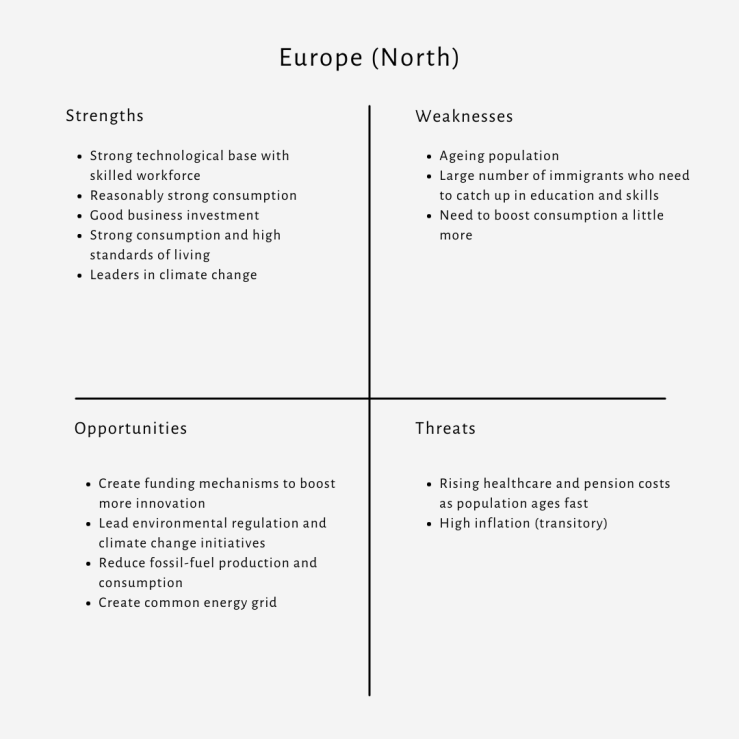

The economies of the West (US as well as both the Europes) need to invest in improved infrastructure, climate change and also need entitlement reform urgently, as their populations age and start putting pressure on healthcare and pension costs. This should accompany tax reform, of course.

These are not merely Covid-related requirements, but those for the longer term. The time when pandemics, climate change and technology will rule our lives for the most part. When economies might be in a sweat (if not in a SWOT), unless we act now.