Since the 1990s, the world economy has been so used to growing along with China, that it’s almost impossible to imagine a world without the Chinese growth engine. That’s because the Chinese economy liberalized in the 1980s and began to trade and do business freely with the rest of the world. They became a member of the WTO in 2001, and since then trade has boomed.

I have been writing on my blog about China’s importance to the global economy, especially through trade, finance and the global supply chain. Its market is also hugely important for most countries that have invested there or trade with it. Three decades later, we are now at a junction where geopolitics and the pandemic have created new pressures, not to mention the Russian attack on Ukraine. To the extent that Trump’s trade war and increased tariffs have receded into the background and nobody wants to discuss them anymore.

It is good to know that in the last quarter of 2021, global trade has grown by as much as 13% over pre-pandemic levels of 2019 according to UNCTAD, even if most of it is accounted for by higher prices and inflation. We have been reading and hearing in the news about the rise in demand for, and supply shortages in shipping containers, as well as a massive spike in energy prices. The war in Ukraine has only created additional pressures in global inflation of food, fuel and metal prices.

The other problem that could impact global growth is that China’s economy is slowing down considerably thanks to new Covid outbreaks and its zero-Covid policy, which the government persists with. China’s importance in the growth of the global economy will start to tell soon, as its lockdowns create disruptions in manufacturing and trade that will impact the global supply chain. As one of the world’s biggest and most important markets for most goods and services, China’s lockdowns and slowdowns will surely affect global growth and the profits of most multinational corporations. How is the world going to fare with one of its most important growth engines not firing at full capacity?

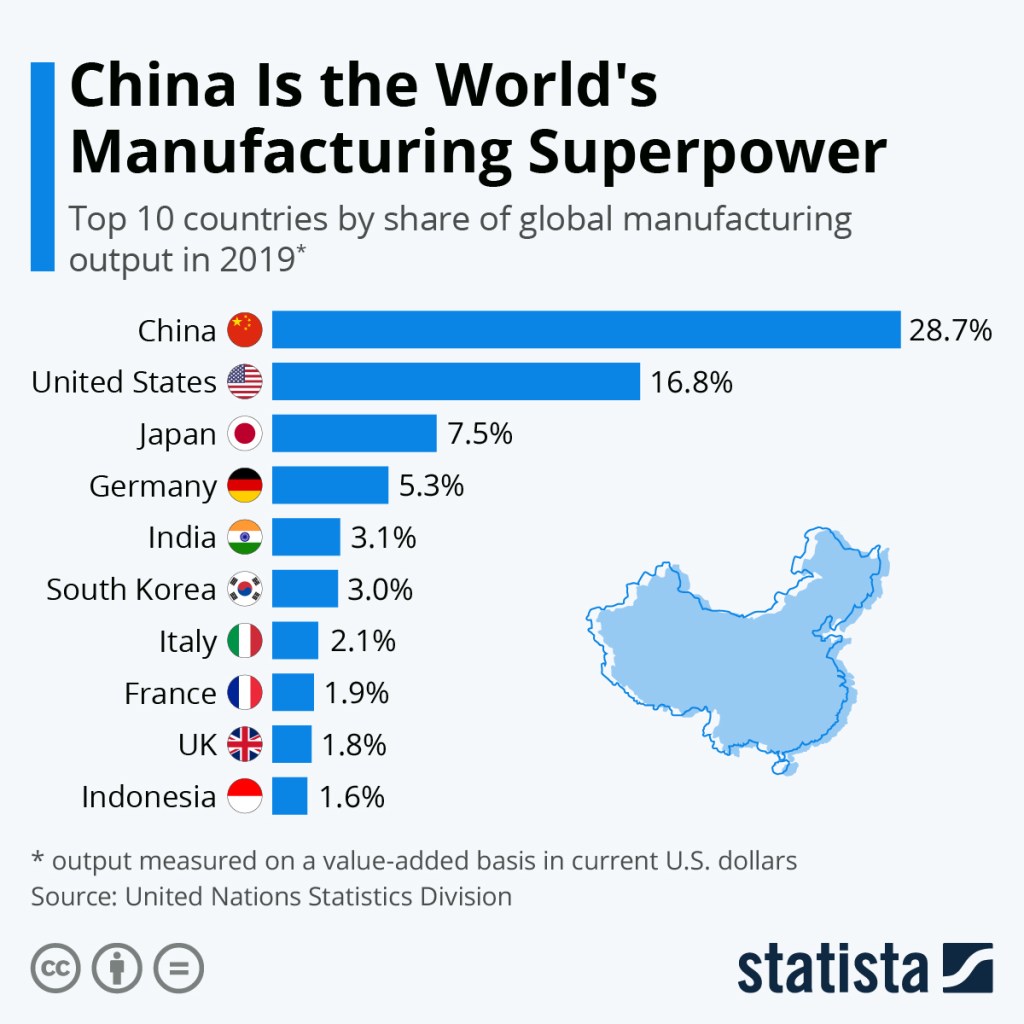

China’s share of global manufacturing according to the UN Statistics Division and Statista was 28.7% in 2019 as the chart above indicates, while its share of international trade (exports) was nearly 15% in 2020. The Chinese government has already recently lowered its annual growth target to 5.5% from 6.5% for the past few years. In the first quarter of 2022, the Chinese economy grew only 4.8%, but better than estimates of 4.4%.

On the one hand, China’s massive demand for commodities will slow down somewhat and perhaps cool down global prices as well, which will be welcome news. However, countries that export commodities to China will be impacted adversely and will have to find other markets to compensate for the losses from China. According to UNCTAD again, south-south trade saw the fastest recovery in 2020, especially south-south trade excluding east Asia. Which means that Latin American and African economies saw a healthy spurt in trade and since these countries trade mostly in commodities, they will now be impacted by the China slowdown.

On the other hand, countries that depend on the global supply chain of which China is an extremely important part, will face severe disruptions in manufacturing and shipping. These will manifest in supply shortages of semiconductors, components and parts especially for electronic products, automobiles, solar panels and perhaps even critical APIs (active pharmaceutical ingredients) critical to the pharma industry as well as higher prices. Countries need to import such products from many other sources as possible to reduce the China slowdown effect and more companies need to invest in the production of these goods outside of China.

I am not in the West-China decoupling camp yet, although recent geopolitical tensions first sparked off by the trade war have certainly contributed to it. And even if the current Covid-related disruptions seem short-term in nature, it would be advisable to take these steps for the simple reason that China is itself concentrating on its domestic capabilities and on indigenization as part of its China 2025 policy. Therefore, there is bound to be a reduction in China’s trade with the rest of the world in the coming decades.

Now, let’s shift focus from China as producer and trader to China as consumer. It is already the world’s largest market for consumer electronics products such as mobile phones and other gadgets, it has the highest internet penetration in the world, the world’s largest mobile payments system, the world’s largest market for automobiles, and is also the world’s biggest EV and EV battery producer. The country has been trying to boost private consumption and its current level of around 39% of GDP is significant, but this doesn’t quite tell you the entire story. China’s middle class has high purchasing power, as reflected in the sales of luxury goods in the country, not to mention the large numbers of millionaires and billionaires. In the latest corporate earnings from the US, it was reported that Starbucks suffered a huge impact from the China lockdowns, and I would imagine many other companies are similarly affected.

These would mostly affect Western advanced economies that depend on the Chinese consumer. This is going to be harder to compensate for, than the slowdown in manufacturing and trade. Companies and countries that have invested hugely in China will just have to wait it out until the Covid pandemic wanes and lockdowns are lifted. Fortunately, India will not be impacted in this area, though we would face severe pressures from the supply chain disruptions and high inflation of parts and components. In any case, India has been trying to reduce its dependence on Chinese goods, though we still have increased trade and a growing trade deficit with them. In APIs, though, India does need to increase investment in domestic manufacture of these critical pharmaceutical ingredients as we have a thriving domestic and export-oriented pharma sector and we cannot depend on China always.

And without an attitude of schadenfreude regarding China’s predicament, we need to seriously consider if India can be a kind of growth engine in the region, if not the world, while we suffer these growth pangs. I don’t think we should approach this idea with arrogance either, but with humility, sincere thought and action. At the moment, India is exporting wheat to the extent that we can without creating domestic shortages and price rises, while the world suffers a shortage due to the supply from Ukraine and Russia being affected. I think in the area of pharmaceuticals and vaccines too, India should continue to supply the world with low-cost medicines. In chip manufacture, we must try and attract foreign as well as domestic investment and create new capacity in the domestic industry as well as for export. India can also boost investment in tea production and export as well as in travel and hospitality within India as well as across the Asian region.

In terms of India as a demand growth engine, we continue to import vast quantities of oil and gas, as well as gold, edible oils, coal, etc. We can never match China’s appetite for commodities, but with emphasis on the right growth areas, India can help to stem the collapse in global growth and trade. Unfortunately, we have opted to stay out of RCEP (Regional Comprehensive Economic Partnership), else we could have finally boosted trade with the region. Recently, ASEAN became China’s largest trading partner and many of those east Asian economies that trade a lot with China will be adversely impacted by the China slowdown. Those that have capabilities in electronics manufacture and global supply chains might cope better.

India, on the other hand, has recently signed an FTA with the UAE and is in similar discussions with the EU and UK in finalizing free trade agreements with them. To be a growth engine of any sort, we need to attract the kind of investment that will help create millions of jobs in the country. High unemployment has become the bane of the Indian economy, and this needs to be tackled on a war footing. Unemployment as well as skill development and training ought to be high priorities. Then, of course, we need to clamp down on inflation and control the pandemic.

Fasten your seatbelts then, for the great economic slowdown is here. It might not be a hard landing, but growth pangs are here to stay for a while. We might as well get used to the idea of China taking a time-out break after having powered global economic growth for the past four decades.

The animated owl gif that forms the featured image and title of the Owleye column is by animatedimages.org and I am thankful to them.