The last time the Western world traded with China and it led to wars, it was of the opium kind, in which India too was involved. That was over a century ago. The opium trade with China and the exploits of the East India Company have since been evocatively recreated for us in fiction by the renowned Indian author, Amitav Ghosh, in his Ibis Trilogy.

One wonders how it will be this time, because never has the world depended on the Middle Kingdom for economic sustenance and growth as in the 21st century. And the financial crisis of 2008 has meant that the West has had to rely even more on China for both direction and growth. China has become a sort of economic barometer, by which to judge, anticipate, plan, prepare and make all sorts of investment and policy decisions.

This is only expected and it is a sign of things to come. Which is why I think the US-China trade spat couldn’t have come at a worse time. It appears to me that the US is having a hard time accepting that it operates in a multi-polar world, that the axis of the global economy has shifted. And it has shifted perceptibly and significantly. Instead of integrating better with the world economy, which willy-nilly means better and more trade and investment with China, the US is putting up all kinds of protectionist barriers and planning more of it.

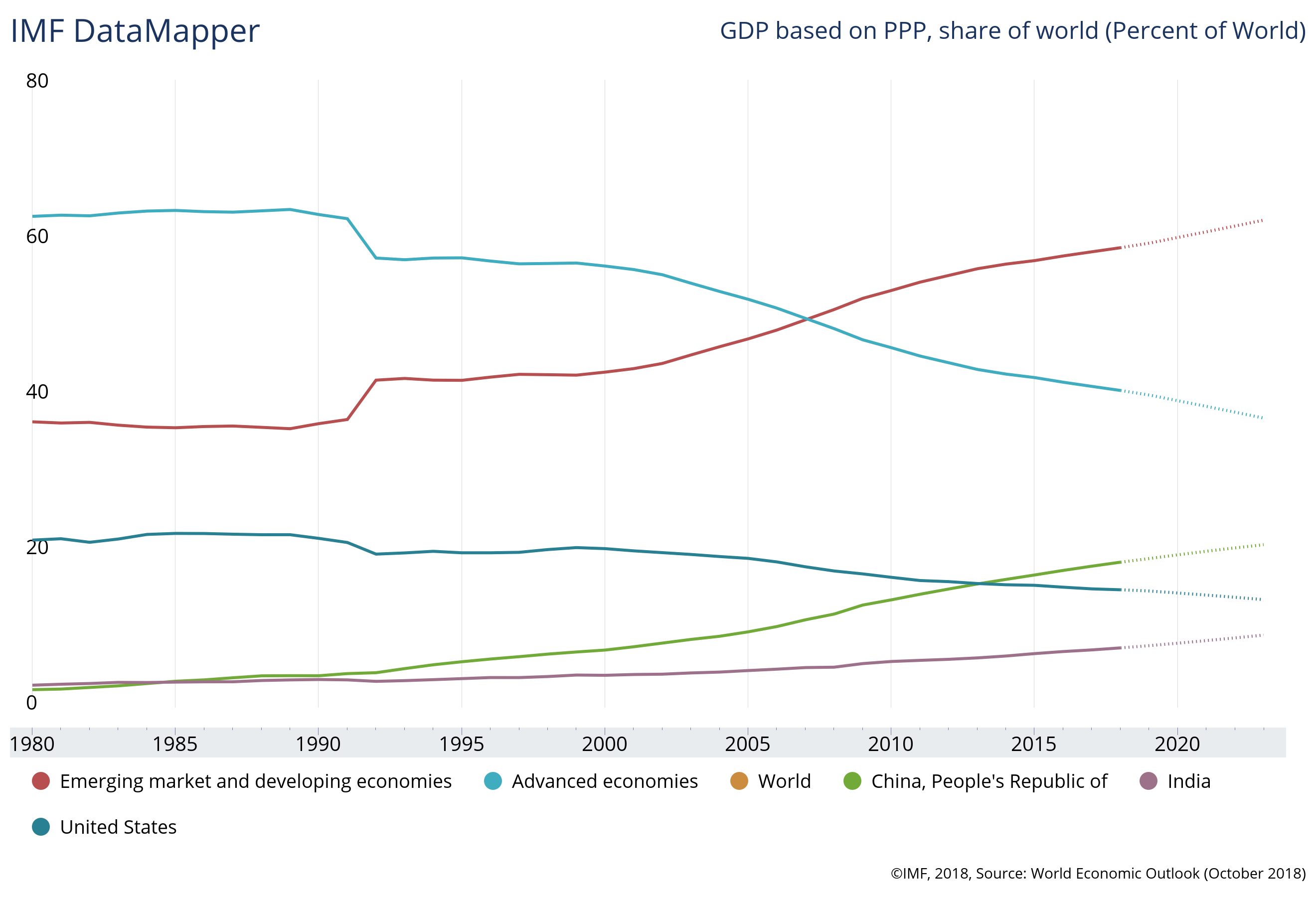

Let us examine a few facts and we will very quickly realise how integrated and important the Chinese economy has become to global growth. More than 40% of global economic growth comes from emerging economies and if we add developing economies to this, 59.77% of global growth comes from these countries. Advanced economies contribute 40.23%. China’s share alone of global GDP growth is 19.18%, while India’s is 7.98%, according to the IMF. The US’s share in comparison is 15.01%. A large share to be sure, but not as large as China’s and that will continue to be the trend for the next half-century at least, if we consider China’s stage of development and the size of its economy.

If we look at international trade, China is numero uno in merchandise exports and number 2 in merchandise imports in 2017. In commercial services, the country is number 5 in exports and number 2 in imports. Taken together, China accounted for 12.77% of total world exports and 10.22% of total world imports by value, in 2017, according to the WTO. Whichever way one looks at it, China’s share of world trade is considerable, perhaps second only to the EU as a trading bloc.

However, the country’s share of exports and imports alone are not enough to really gauge China’s importance to global growth. Because of China’s model of economic development, most of the trade is tied to investment in the country’s economy. Foreign trade and foreign investment in industry go together in China, so it is important to look at FDI in China. As Arthur R Kroeber, Senior Fellow at the Brookings-Tsinghua Centre and Head of Research at Gavekal Dragonomics, an economic research centre, notes in his book, China’s Economy, What Everyone Needs to Know:

A feature of China’s industrial development that sets it apart from its East Asian peers is the large role of FDI… From 1985 to 2005, annual FDI inflows averaged nearly 3% of GDP, a very large number. For South Korea and Taiwan during their comparable high-growth eras (the early 1970s to the early 1990s), FDI inflows were only about 0.5% of GDP. And in Japan from the mid-1950s to the mid-1970s, FDI was basically nonexistent, running at less than 0.1% of GDP… The role of foreign companies is particularly noticeable in China’s export trade… since the early 1990s, a third or more of exports were produced by foreign-invested firms and the foreign share peaked at 58% in 2005. For exports classified as high technology by the Chinese government, the foreign role is even larger: from the early 2000s until 2012, well over 80% of high-tech exports from China were produced by foreign firms and the foreign share is still around three-quarters.

Let us look at FDI in China. According to the latest report from Reuters this year, Chinese FDI rose 3% to US$ 135 billion in 2018. This has perhaps been the slowest pace of FDI growth in China, but the overall annual inflow at US$ 135 billion remains very significant. However, since this FDI and Chinese exports are closely aligned with the financial performance of most multinational corporations, it has a direct bearing on the GDP of countries from the US and UK to France, Germany and many others across the world. As The Economist notes in its issue titled “Slowbalisation”, the share of global profits of multinational firms among all listed firms has dropped from 33% in 2008 to 31% in 2018. Besides, overall FDI has tumbled from 3.5% of world GDP in 2007 to 1.3% in 2018.

Meanwhile, Chinese outward investments have continued to grow, linking up parts of the global economy further. Although Chinese FDI into the US dropped dramatically in 2018, it has grown in other countries, notably in Europe. This latest spurt of Chinese investment into Europe during the height of the financial crisis provided some of the ailing economies of southern Europe much needed respite, such as the Chinese investment in Greece’s largest port, Piraeus, but it has also caused tensions between European countries, especially among those that perhaps fear a Chinese “takeover”.

If the US is obsessed with a large and looming trade deficit, Europe fears selling out to China! Needless to say, most of these fears are unfounded. As Volvo, the Swedish car company has recently been finding out, the brand is rediscovering its Swedish roots and heritage all over again under Chinese ownership and management control. It is worth mentioning here that Chinese FDI into Sweden spiked by around 300% in 2018 and most of the investments were in renewables, clean tech, electronics and communication technology.

China clearly has plans for the future. And they seem to go beyond One Belt One Road investments in infrastructure, linking the East to the West, by land and by sea. China would clearly like to focus on high-technology investments. It already leads in 5G technology, solar energy, mobile payments, electric cars and is second to the US in developing AI, but not trailing by very much. The country is also extremely focused on developing indigenous technologies and with its growing talent pool of highly educated and trained research engineers and scientists, it will give advanced economies stiff competition.

Scott Kennedy of the Centre for Strategic and International Studies gives us the salient features of China’s “Made in China 2025” policy which, he says, is close to Germany’s “Industry 4.0” plan which aims at industrialization through greater use of information technology. Besides the focus on IT-based industrial development, Made in China 2025 also aims to increase the indigenization of manufacturing components to 40% by 2020 and to 70% by 2025. There is also a greater emphasis on conforming to and setting international standards and best practices than before, which should augur well for multinational corporations doing business in China. The world needs to move cautiously, but against this backdrop, we might also need to re-examine calls to boycott companies like Huawei, for example.

As the second largest economy in this part of the world and the fastest growing, India too has plenty to gain from engaging with China. China is our largest trading partner, and trade between the two countries is growing, but it is mostly one-way, with massive and cheap Chinese imports flooding our markets, ranging from steel to electronic components to almost everything you can think of, including critical ingredients for our highly successful and much touted generic pharmaceutical industry. India’s trade with China is around US$ 80 billion, with the deficit at around US$ 33 billion. We don’t seem to have a policy to deal with it, save for raising import duties; none of it has had much effect so far. Chinese handset manufacturers have all but edged out Indian companies and are second only to a Korean brand, Samsung. If India doesn’t move quickly and efficiently enough on electric vehicles, we will soon find ourselves swamped by car brands from China. Not even Maruti Suzuki might be able to withstand the onslaught. And while on the subject of cars, JLR is having a rough time in China, not just with higher import tariffs but with product quality issues. There have been massive product recalls in China and a few reports of angry Chinese customers thronging the company’s headquarters in Shanghai. While the incident has largely gone unreported in most sections of the Western media and is altogether absent from Indian media, it tells us something about the Chinese consumer. That we can’t take them for granted anymore; that they are becoming much more discerning and no longer in thrall of international brands, they are buying Chinese cars.

This is a new and assertive China that we have to accept in our midst. And in such a highly interconnected and globalized world of business, with so much at stake, can countries really afford to put up walls and barriers to trade and investment? Do we not risk much more by obsessing and quibbling over details and losing sight of the bigger picture? Every country looks out for its own economic interests, but where should one draw the line between short-term political expediency and long-term economic gains? With the recent IMF forecasts for global growth as well as for individual countries, that make for grim reading, can our leaders not see the writing on the wall? That China is the world’s second largest economy and that it will soon be the largest economy in the world, no matter what?

China has plenty of economic issues to deal with, domestically. They have cut income taxes, relaxed some bank lending (over US$ 400 billion in January alone) and increased investments on infrastructure once again. With already astronomical levels of debt, there are also widespread concerns over China’s US$ 4.5 trillion local government financing vehicles’ debt (which doesn’t reflect on their books as fiscal deficit) in order to pump-prime the economy. While one cannot say with any certainty how successful any of these attempts will be, one thing is clear: that the world economy, led by the US, is inextricably linked with China’s and world growth is dependent on how China does.

One hopes for a quick resolution between US and China on their ongoing trade talks, because with so much foreign trade and investment at stake, neither country can afford to walk away from the negotiating table. What’s more, it has huge implications for the rest of the world. One also hopes that Europe will find a way to deal with China’s rise and work with their trading and economic partners, rather than raise the bogey of Chinese takeovers.

These long, protracted talks between the world’s two leading economies have already taken way too long. The longer the world waits, the longer it will seem like global growth is on a slow boat to China. One only hopes it will not be like the Ibis, this time around.

I will be sharing a link to a talk by Martin Jacques on understanding China’s rise in the May reading selection at The Whistle Library on Peripatetic Perch exclusively for subscribers to The Whistle newsletter.