More than half of 2025 is over and we’re almost about to enter the last quarter of the calendar year. It’s time to assess which way the global economy is headed because the last time I wrote about it, it was just after the IMF and World Bank Group Spring Meetings in the US in April this year.

More importantly, how is the global economy withstanding the Trump tariffs? And how are countries managing their public finances as well as inflation? I suppose considering the tariffs were fully announced only in August 2025, and even now countries are said to be in negotiations with the US, it’s too early to tell the effects of the tariffs just yet. What is clear is that no country is retaliating with reciprocal tariffs of their own and even China which did announce retaliatory tariffs, has agreed to reduced tariffs for another 90-day period. Very few countries can truly retaliate as I had written earlier, China being one of them.

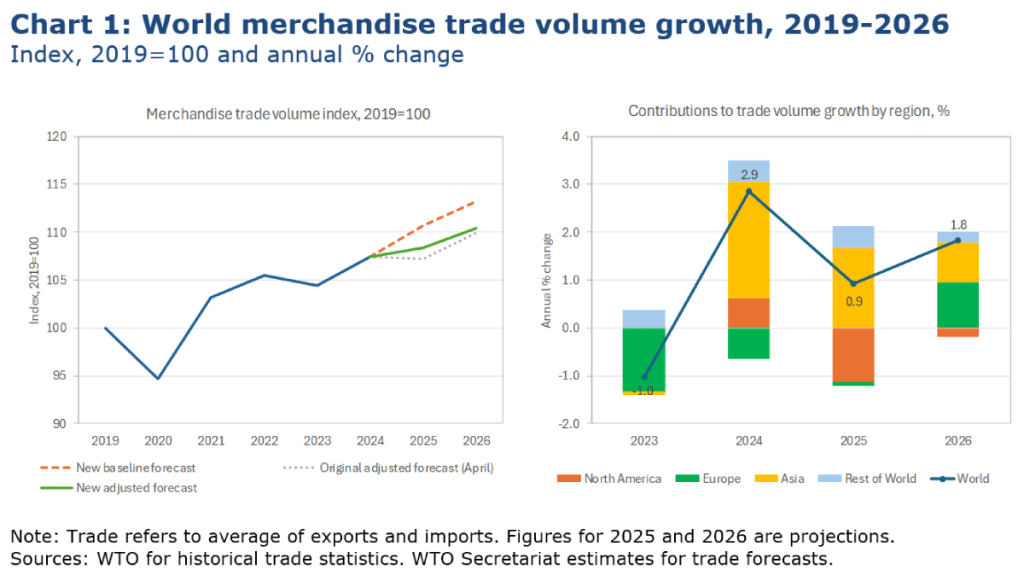

While it might be early days yet, it is believed that the higher tariffs have begun working their way into higher prices for some goods in the US, as CPI figures for July showed. Federal Reserve Chairman, Jerome Powell said as much himself in his speech at the 2025 Annual Jackson Hole Symposium held recently in the US. Still, everyone expects that the Federal Reserve will cut interest rates in September 2025 by 25 basis points or a quarter of a percentage, which they have. They now have the benefit of another month’s CPI reading before their decision. August CPI in the US came in higher at 2.9% year over year, and the core remains high at 3.1% year over year, same as in July 2025. The larger companies in the US have probably not yet started passing on higher tariffs to consumers, but in the corporate earnings for the June 2025 quarter, all the three US automotive giants, GM, Ford and Stellantis mentioned significant hits to their earnings – to the tune of billions of dollars and more – on account of higher tariffs. Their case is even more complicated, since car manufacturing in the US involves two other countries – Canada and Mexico – who are part of USMCA renegotiated by Trump in his first term, but now tariffed as well. According to the WTO, global trade faces significant risks from tariffs and geopolitical tensions going into 2026, even though the world has avoided the worst so far thanks to pauses and measured responses.

I think the bigger problems facing the US are its large fiscal deficit and its debt mountain, which I had written about in a blog post recently. As they also are in UK and in many countries in Europe. In fact, the fate of the beleaguered French government hung on the vote of confidence in its revised budget proposing massive cuts that are indeed required in its public spending. The French government lost the vote of confidence in parliament and the country is in a state of chaos once again as protests break out over the new prime minister’s appointment. In the UK, it is widely anticipated that the UK Chancellor will have to raise income taxes in the Autumn Budget this year, as the British government tries to control the fiscal deficit as well as the debt. The UK and Europe managed to grow their economies in the June 2025 quarter and with the resetting of the trade relationship, trade between the two will be smoother and better. However, Germany, Europe’s largest and most powerful economy could still be in recession territory for the third consecutive year. As it transitions to a new and different kind of economy it is also having to face the brunt of reduced international trade, first with China and now with the US.

If we consider consumer price inflation, it is still high in many countries around the world even as it is on a downward trajectory. For the most part in developed economies, it is quite entrenched in services inflation and in housing, with core inflation higher than the headline inflation. This is a feature in India as well as in Japan and the UK. Within Europe, eastern European countries seem to have higher inflation and some of this could be because they are the faster-growing economies, especially those in the Balkans. In countries such as Turkey and many in Latin America, including Argentina and Venezuela, inflation is still mind-bogglingly high and raging.

Therefore, inflation is not completely under control in many countries around the world with the reasons for inflation varying between developed and developing economies. Yet, central banks everywhere seem to be under pressure to lower interest rates so that the cost of capital comes down. In developed economies such as the US, it seems to be political pressure driven by a social need: to bring housing mortgage costs down especially ahead of the mid-term elections next year. Central banks are in a quandary in these economies where they are taking a calibrated approach to bringing down inflation. If they lower rates and take an accommodative stance, what about the already high fiscal deficits and debt levels? It requires a balanced approach with central banks and governments working in lockstep with each other to ensure that economic growth is not hampered and that price stability is also maintained.

This apprehension is most visible in bond markets across the world. In recent weeks and months 10-year bond yields have risen appreciably in most major economies, telling governments and central banks that the cost of their borrowing is going to be high. The markets seem to be cautioning governments that their fiscal and debt positions are going into danger territory, and that they will demand more for their money. In India too, the 10-year bond yields have risen in recent weeks, although India’s fiscal deficit is already on a reduction path – from 4.8% to 4.5% of GDP and our current account deficit too is low at just -0.9% of GDP. I suppose the creditors anticipate that the Indian government might slip on its fiscal deficit target this year because of the government having to offer financial assistance to exporters on account of the US tariffs, as well as lower tax revenue thanks to income tax breaks as well as GST relief just recently announced.

Rising bond yields and the rising price of gold together can and should be cause for concern. Though central banks themselves are said to be bulking up on gold purchases. Meanwhile stock markets seem to be on a steady rise through the year, albeit with volatility. In the US, it is reported that a lot of the rise has come from big tech companies’ stocks especially with their AI plans. Their corporate earnings too have been good in the June quarter, though one wonders how much of this can be sustained with a slowdown in economic activity and growth expected in the months ahead and perhaps even next year. If higher tariffs are passed on to consumers in the US, one can perhaps expect good and even better earnings to continue for a while on the back of higher prices. This would vary from industry to industry, of course, and on the specific consumer segments being addressed. But for how long? Sooner or later, consumers will press the brakes and slow down consumption, triggering off weakness in business performance and the laying off of employees and workers.

The question is how much of the economic slowdown induced by Trump’s tariffs, can be offset by a growth in productivity thanks to AI. I am an AI sceptic – especially of generative AI – but I think that even if AI improved productivity, it would come from very small and specific pockets of industry in the near future. Not the kind of widespread surge in productivity and efficiency that computers ushered in the 1950s and 1960s in advanced economies, especially in the US. Looking at the soaring stock market valuations of some of these tech companies, I wonder if we aren’t already seeing the beginning of an AI-based asset bubble.

The effect of AI on the jobs market and on employment in general is also important to consider. Already several large tech companies in the US have been laying off people since the start of this year and I think many, if not all of them, would have to do with how AI is changing their own businesses. In most developed economies where we are already seeing an ageing demographic and anti-immigration sentiment and policies, the prospects for many people to find work and for these economies to grow, is narrowing. This might send businesses rushing to AI and technology even more than before, setting off another wave of employees and workers losing their jobs.

In large economies such as India, China and Brazil, a lot of economic activity is labour-intensive, but this doesn’t mean that employing technology in industry in these countries is low. Besides, these economies have large domestic markets to cater to, which means generating good quality and well-paying jobs are imperative. Besides the growth in employment generation, these countries also need good wage growth. And since large sections of the economy at least in India operates in the informal sector, good wage growth is probably a rarity. This remains one of the biggest economic challenges in India. Hopefully, these economies will be able to weather the tariff hikes better than many others that are much more dependent on exports.

In Africa and Latin America, their various trade blocs within their continents and with other nations elsewhere ought to help them increase trade, investment and economic cooperation. They do need outside help of course, as many countries in Africa and Latin America are also the source of a lot of migration to developed economies in recent decades. This is why the Global South must increase and improve dialogue, investment, trade and economic ties. Not merely for the mineral wealth and natural resources that many of the African and Latin American countries possess, but for helping these economies build their own domestic capacity and grow.

In the context of recent geopolitical tensions, some brought on by wars and others by trade and tariff wars, I fear that many countries will be forced to take positions opposed to what they have always stood for. And I am concerned that in this West vs East paradigm that seems to be emerging, or the way the media too frames it, we might all lose out on the economic growth that is to be had if we all worked together. The recent meeting of several countries at the SCO, and especially the Russia-India-China triad was being billed as the response of countries opposed to the West. I have never seen the SCO being given so much importance on Indian as well as international media in earlier years, and I suspect unprofessional PR agency idiot bosses were responsible for the lavish media coverage this time.

I had written on how India ought to raise its level of participation and engagement at the SCO in a blog post, because I believe that the Central Asia region is one of economic growth and relative peace, because of the former. India must invest in this region and participate in its economic growth because the region is also of strategic importance to us. But this narrative of the world being split into pro and anti-US or pro and anti-west forces, or that the Global South is anti-west is dangerous and mischief-mongering. Similarly, I hope that in the sudden “swadeshi” (national) lurch that my own country, India, is taking we do not turn protectionist in our policies. Nor should we unleash an anti-MNC, jingoistic-nationalist wave across India. It would hurt investment and trade with India even more than the US tariffs, and would have a deleterious effect on our economy, just when it might be on the upswing.

Whichever way the global economy is headed, every country has to navigate the turmoil carefully and with a view of the long-term. India too has to tread carefully through the geopolitical tensions and maintain cordial relations with all countries. The wars raging in Ukraine and in the Middle-East will test our allegiances, but I think our greatest strength as a country is to cooperate and work with all, but be a slave or lackey to none. I think we might have overextended ourselves in thinking that we can solve the world’s problems, and it would be wiser to keep our heads down and stay focused on our own economy in the near future.

The featured image at the start of this post is by Nicole Wilcox on Unsplash