The world’s most powerful financial elite, comprising finance ministers and central bankers converged in Washington DC last week for their annual Spring Meetings with the World Bank and the IMF. This follows on from the US elections last November where Trump was elected US President for the second, but not consecutive term. Usually, this wouldn’t be of great consequence. But since President Trump has announced a new tariff regime on the rest of the world, it ought to and will impact how the global economy fares this year, and in the years to come.

A cursory glance at the IMF and WB Group meetings schedule and there wasn’t even a hint at anything like the Trump tariff impact was on the agenda. Perhaps this is just one more way the Washington Consensus maintains its calm hold on the world – by pretending everything is normal and that nothing has changed. I don’t want the world obsessing over the tariff hikes to the exclusion of everything else, as I just wrote in an Owleye column, but the financial elite of the world must discuss it, surely. Maybe and hopefully, they will, quietly behind closed doors.

From what I think is still the most important issue facing the world, it is consumer price inflation and its trend through the year. In the face of steep tariff hikes and retaliation, most economists expect CPI to rise, especially for American consumers. Even without the tariff hikes, the world has to tread cautiously in managing inflation, since it has the biggest impact on the poor and economically vulnerable. In advanced economies and even in India, we have begun the interest rate reduction cycle since CPI has been decreasing. Though core inflation is still at elevated levels, and central banks have to be watchful. Thanks to climate change and the wars still raging consumer price inflation is likely to stay stubborn.

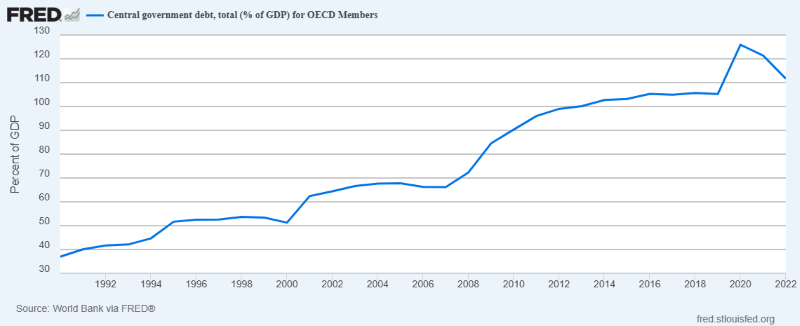

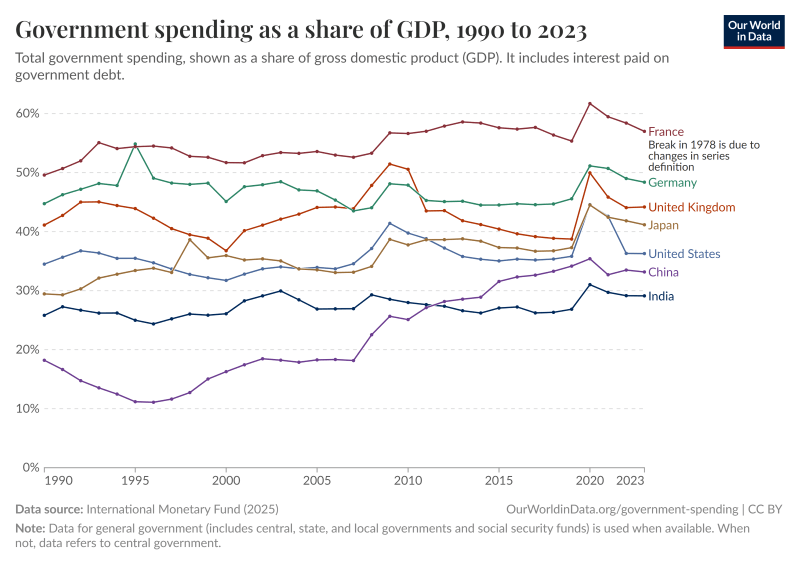

Next, fiscal deficits and public debt levels around the world are still a huge problem. Even advanced economies have huge fiscal deficits and mountains of debt, especially the US, UK, France, Italy, Japan and China. Many might wonder why I am including China in the grouping of advanced economies; I think it has all the characteristics of a large, rich and industrialised economy, except perhaps in per capita income terms and I think this is an anomaly due to its large population. The problem is not the fiscal deficits or debt levels alone, but the prospects of the government having to rein in spending at a time when the global economy is still fighting off inflation and is engaged in a very fragile economic recovery.

Then, there are massive supply chain disruptions to be expected as a result of Trump’s tariffs and companies as well as governments around the world will have to navigate their way through the uncertain months and years ahead. I think that the diversification of supply chains that began post pandemic must continue, and that the world will have to become less dependent on the US. In fact, as I have been writing on my blog, countries and companies will do well by diversifying their exports away from the US to other markets.

Global trade will slow down as a result of Trump tariffs and the most recent WTO report highlights the risks to global trade from restrictive trade policies, especially the reciprocal tariffs. If they go into effect, WTO estimates that global trade will slow by 1.5% in 2025. Even as President Trump was taking office, the European Commission President Ursula von der Leyen had announced at the WEF Davos Summit that Europe had negotiated a new Mercosur trade deal with Mexico and with Latin America. Indeed, it will help if the EU increases its trade engagement with all of Latin America.

I think that smaller, developing and even emerging economies would do well to negotiate trade arrangements with larger, regional trading blocs, as they need the heft of large trading blocs to grow their economies in the face of slow economic growth and Trump’s tariffs. On the other hand, larger countries ought to concentrate on their domestic economies, and focus on easing bottlenecks as well as implementing and deepening policy reforms. I see India in the latter group that ought not to get fazed by the Trump tariffs, but focus on economic policy reforms and creating better quality employment. There are many economic commentators who are of the view that Trump tariffs might be a blessing in disguise for India, in the sense that it might force the Indian government to reduce import tariffs on a whole gamut of products. I would agree, but with a caveat that it shouldn’t be done because the US or anyone else is forcing us to. And if we reduce import duties on any goods, it ought to be with careful consideration and a long-term view of strengthening our strategic position and becoming more competitive.

I think countries in the African continent too ought to be focused on resolving their conflicts so that greater foreign investment can take place. They are also better off pursuing trade arrangements within the continent through their trading blocs and with the rest of the world. China is already the biggest investor on the continent, though its mode of investing through cheap credit makes it very risky and other countries and regions from Europe and UK to Japan and India must also step up their economic cooperation and trade and investment with countries in Africa. From all my reading, I am of the impression that African countries lack a large enough regional trading bloc with either the Global North or the Global South. This might be because African countries’ leaders – especially those of the past – have themselves preferred bilateral trade arrangements, where they can exercise greater control over their countries’ economic future. This has usually led to huge cases of corruption involving the political leaders and has rarely benefitted the common man in African countries.

The big elephant in the room is of course, higher tariffs, which is why the World Bank Group Meetings must discuss its impact and how to navigate the waters better. If this does cause inflation to tick higher, not just in the US but in all major economies because of retaliation, we might have to envisage a period later in the year when central banks that are on an interest rate cutting cycle could have to reverse course. This would necessarily raise borrowing costs for businesses and households as well as for governments, at a time when growth would be slowing even more than now.

Many economists have been talking up the possibility of a recession in the US later in the year, even if a short and shallow one. Some are of the view that even if recession doesn’t rear its ugly head, a period of stagflation could be on the cards. Besides the immediate economic impact, there is the longer-term effect as well to consider: governments who are already under strained public finances being forced to rein in their spending further. A period of fiscal austerity would be the worst thing in circumstances that put the middle-class consumer and the poor and unemployed under tremendous pressure. This is because we aren’t done yet with controlling inflation arising post-pandemic even after three years.

The other fallout of governments having to tighten their belts in times of a severe economic slowdown or recession, would be political. As it is we have the far-right populist political parties making huge gains in elections over the past two to three years, especially in the western, advanced economies. Already many of these governments in Europe and in the UK have had to increase their defence spending as a percentage of their GDP. And in the process of doing so, they have had to cut public spending elsewhere, as in the UK and in France. France had a contentious budget over which the newly appointed Prime Minister had to resign and there is a lot of opposition to the cuts in public spending as well as the pension reforms. Germany’s newly elected CDU-led government has been able to agree with its coalition partners on an economic plan that is focused on boosting growth, as the country has been in recession for more than two years. The biggest challenge for Germany is to pivot their economy to the new industrial economy that is led by digital technology. Fortunately, they seem to have the fiscal headroom to be able to carry out economic reforms and follow an ambitious growth target.

In fact, Europe needs to stay the course of economic reforms as proposed by Mario Draghi’s report to improve their competitiveness. Ideas like investing more in digital technology capabilities, and unifying their capital markets must be implemented as soon as possible. Governments will have to find the money to finance these large initiatives even as austerity bites in certain member countries, were inflation to rise again.

When policy choices are limited, and at the same time imperative, governments in many countries will have to do a fine job of prioritizing the right areas for action, make the most sensible long-term policy decisions and most importantly, convey to the markets their commitment to adhering to these policy reforms. Only then will countries attract long-term investment of the kind they need.

Speaking of capital markets, they have been in turmoil since the start of the year. The volatility is unprecedented, with gold the only big gainer among asset classes. This is not a good sign in economic terms, and the US which has the world’s largest stock-markets by capitalization as well as the largest debt markets, needs to seriously consider the fallout of its policies. In the last quarter of 2024 and early this year, the Chinese stock-markets were reported to be doing really well, although that has been tempered by the Chinese government’s retaliatory move on tariffs, I suppose. I think Europe could be the big gainer in terms of investment, if it manages to implement the right policies soon enough. I was thinking that even in terms of human capital, the best and brightest minds working on scientific research and innovations in the US in academia and in research institutions might consider moving to UK and Europe, if the Trump administration continues its attack on universities and institutions of higher learning.

I think India and many other emerging economies in Asia and Latin America will do relatively better, both in terms of attracting investment and in terms of carrying out much-needed policy reforms. Here the bigger challenges are of generating large and better-quality employment, improving the earning and spending capacities of people. I think that India and all of south-east and east Asia will do reasonably well, even in the face of Trump tariffs. Some of the countries that Xi Jinping visited recently such as Vietnam, Cambodia and Malaysia have been hit by very large tariff increases and they all have considerable exports to the US. But they also trade a lot with China and I am not sure they will pick sides in what is essentially an economic and trade war between the US and China into which the whole world is once again being drawn.

At the time of completing this piece, IMF had released its latest April 2025 World Economic Outlook, and I must say that they have done well to acknowledge the risks to global growth from raising tariffs and have accordingly revised downward their growth forecasts for the global economy. The introduction to the report says, “Intensifying downside risks dominate the outlook, amid escalating trade tensions and financial market adjustments. Divergent and swiftly changing policy positions or deteriorating sentiment could lead to even tighter global financial conditions. Ratcheting up a trade war and heightened trade policy uncertainty may further hinder both short-term and long-term growth prospects. Scaling back international cooperation could jeopardize progress toward a more resilient global economy.”

I am not sure about the subjects chosen for the chapters of the April 2025 WEO, as they seem to be motivated by unprofessional PR agency idiot bosses from India who have been meddling with IMF as with other international organisations such as the OECD. I would have thought that the more urgent and pressing need is for economies to be able to generate good quality employment while adopting technology and AI, as also staying focused on climate change commitments. That said, the executive summary of the WEO is a better, more relevant and important read.

Hopefully, better sense will prevail and there will be a rollback of the reciprocal tariffs by the US, as well as a reconsideration of the trade relationship between US and China which affects the entire world. Discussions and negotiations are the only way forward, not bullying tactics and threats.

The featured image at the start of this post of people crossing a city street is by Vlad B on Unsplash