What? There are no ‘I’s in the global economy, of course. Well, the year has begun with corporate earnings and once again it’s time to turn our attention to these to see what they seem to be telling us about the health of the economy. India’s, and the world’s. From the corporate earnings announced, they already seem to be indicating a couple of broad trends for the year.

The first is that interest rates will have a huge bearing on corporate earnings as well as the economy. With central banks raising interest rates in an effort to combat stubborn inflation, banks are reporting a good set of earnings as they benefit from higher interest rates. Besides, with stock markets still buoyant in many countries despite monetary tightening, US banks such as Goldman Sachs have reported good growth in equity trading incomes as well.

In India too, banks are reporting better earnings and more importantly, their asset quality continues to improve with each quarter. Unfortunately, it’s the retail loans that are growing while corporate lending remains muted. That could mean several things. That demand for business credit is low, that large companies are able to raise money in the capital markets, and finally, that business investment is itself low. I think it could be a combination of all three factors, and I will return to the last point about low business investment a little later in this piece.

The second broad trend I see is huge investments in technology, especially of the AI kind. We have already seen US big tech stocks rally for most of 2023 on the back of expected growth through AI capabilities, and 2024 has begun with a rally again, this time in response to earnings. Microsoft, in particular reported a stellar set of earnings and so did Google and Meta. Even traditional tech giants such as IBM reported a good set of earnings and Intel also reported its first growth in revenue in many quarters, and a higher net income but guided lower for the first quarter of 2024. In contrast, Apple reported a decline in revenue and net income for December 2023 quarter, mostly affected by production problems in China due to Covid lockdowns. And Amazon reported a good set of earnings thanks to holiday shopping and cost-cutting measures in the form of employee layoffs.

On the other hand, Indian tech companies have reported a muted set of earnings for the December 2023 quarter, citing overseas clients cutting back on tech spending. We will have to wait and see for a couple of quarters whether this improves or not, but something tells me that there might be a more fundamental shift taking place in the kind of tech investments companies across the world are making. And if it is more of the AI kind and intelligent cloud where Indian big tech companies don’t as yet have the expertise or capabilities, we might fall behind in the tech sector. One hopes this is not the case, but it’s time our tech companies move up the value chain, especially in cloud and AI.

Of course, after the hiring spree by US tech companies in 2021 and 2022, last year they began to lay off workforce in large numbers. 2024 too has begun with large layoffs announced and more to follow, but this time it appears to be due to structural changes in companies as well as AI. We have not seen this level of retrenchment in the Indian tech industry even though hiring seems to be muted, except for several senior level exits at Infosys. The difference is that the US economy is still hiring in large numbers and even the latest non-farm payroll data that was announced was a huge surprise at 353,000 for January 2024. India’s long-term problem with high unemployment continues to bother the economy, especially as we are an economy with many more millions of younger, working age population.

The third broad trend that will play out at least through the first half of 2024 is inflation and consumers’ response to it. Though consumer price inflation is ticking down at varying paces in different parts of the world, prices of most goods are still high and consumers are clearly feeling its effect. From the few corporate earnings announced so far, it appears that consumers are cutting back on discretionary purchases while continuing to spend on essential goods and services. P&G’s earnings for the last quarter were good because of maintaining higher prices, while volumes in many markets, across segments, were either flat or declined. In India, leading CPG companies such as Hindustan Unilever and ITC also reported flat revenue growth and margins too seemed to be under pressure, what with volume growth for HUL at a mere 2%. I think management of both companies cited weakness in rural demand as one of the main reasons for the muted earnings in the last quarter. While rural demand has improved from its lows of the previous years, it is still being impacted by high inflation. I think CPG companies have still not begun passing on the benefits of lower commodity costs to consumers and are beginning to feel the adverse impact of higher prices, along with consumers. ITC might have reported a higher profit growth of almost 11% because of its hotels and cigarettes businesses, and it is also reported to have benefitted from higher other income as well as a lower tax expense during the last quarter.

Despite discretionary sales being weak, the long festive season in India seems to have helped boost the sales of automobiles and branded jewellery. These seem to be doing well, although we must remember it is among the higher income classes in urban India. Domestic sales of passenger vehicles in April-December 2023, was 30,83,245, according to SIAM (Society of Indian Automobile Manufacturers) with the festive season accelerating the sales in October-November 2023. However, the previous year’s (2022-23) domestic sales of passenger vehicles came in at 38,90,114, so we will know if FY 24’s domestic sales grew over FY23 only at the end of this quarter. That said Maruti Suzuki and Tata Motors reported a good set of earnings in the last quarter. While the former who is also India’s largest carmaker is focused only on passenger vehicles, the 33% growth in net profit as well as 14.5% growth in revenue over the previous year does indicate better realisations on newer models. Tata Motors on the other hand has benefitted from being the first mover in electric vehicles in India and their earnings were also hugely boosted by better performance from JLR as well as the commercial vehicles business accelerating.

Meanwhile, Titan Company’s earnings for the December 2023 quarter were also good, thanks to the festive season and the wedding season in India, even if the net profit came in below estimates. What are still not seeing robust growth are appliances and consumer electronics, with mobile phone sales remaining muted through the last festive season. On the other hand, of course, we have Apple production out of India and its sales – mainly exports – soaring.

If we look at the overall Indian economy picture, we are one of the faster-growing economies in the world. Our Q2 FY24 GDP growth came in at 7.6%, but some of the salient features of this growth is that private final consumption growth slowed to 3.13% year over year and its share of GDP too declined from 59.3% in FY23 to 56.8% in FY24. It tells us that there is weakness in consumer spending and Q3 earnings from CPG companies seem to corroborate some of this, especially the weakness in rural demand. On the other hand, gross fixed capital formation grew in absolute terms by around 11% in Q2 FY24 and its share of GDP too increased from 34.2% to 35.3% over the previous year. While this might look promising, I think most of it is probably due to government investment with their huge increase in capex during the year, and private investment is probably not so buoyant, despite all the PLI schemes. I think it’s time the NSO provided more granular data on the composition of GFCF between public and private sector and also between business investment (whether green or brown) and infrastructure projects, including housing.

We have the Indian parliamentary elections due in a couple of months and ahead of that, the government announced its interim budget a few days ago. It was not the usual vote on account kind of budget, and it seemed to indicate how sure this government is of returning to power for its third term. The interim budget seemed to squarely focus on fiscal consolidation, which is very much needed in the context of the huge borrowing and spending that the government had to do during the Covid years. The fiscal deficit for FY 24 has actually been brought down to 5.8%, lower than the targeted 5.9% of GDP. The government has managed this through cutting public spending by around Rs 1 lakh crore over the budget estimates for FY 24 and through higher total tax revenue receipts. The growth in direct taxes, especially income taxes collected over the previous year is a good and encouraging sign and GST collections too continue to improve, though I think we need to adjust the latter for inflation.

The budget also seemed to hint at a sharper focus on clean and green energy, with solar energy and green hydrogen, etc. A Rs 1 trillion fund was also announced to incentivize deep research in the private sector, by making available 50-year interest-free loans, though details are sketchy at the moment. I think the government needs to clearly specify the areas of research which ought to lead to new technologies being developed, rather than the funding of new start-ups. The latter already has several avenues for attracting investments and several funds that provide venture capital, such as the 100 Billion Vision Fund backed by SoftBank.

The government is promising to focus on four groups of people who, it says, needs greater attention. These are the poor, farmers, the youth and women and the budget outlined social spending schemes to help each of these beneficiaries. While this is good, more emphasis needs to be placed on creating good and large employment opportunities in India. Else, all this spending is just income redistribution without it leading to better jobs and livelihoods for vast sections of Indian society. Which brings me back to the government spending on education and basic healthcare being inadequate. In fact, even in the interim budget many of the areas where the budgeted amount for FY24 has not been spent, fall under these kinds of heads, as you can see from the outlay on major schemes document from the Ministry of Finance website. In my blog posts, I have often highlighted this tendency to not spend even what is allocated in the budget on education and healthcare and this has grave consequences. It is not enough to focus only on IITs, IIMs and AIIMS; we need to improve the quality of primary and secondary education as well as its availability in remote corners of India and do the same for healthcare. If we keep cutting back on spending on critical areas of development of human capital even as our GDP grows at faster rates, it means we are spending ever smaller shares on things that matter most.

The interim budget does increase government capex for FY 25 once again, but by a more moderate 11%. This is perhaps because they expect private sector investment to take more time to pick up pace during the year.

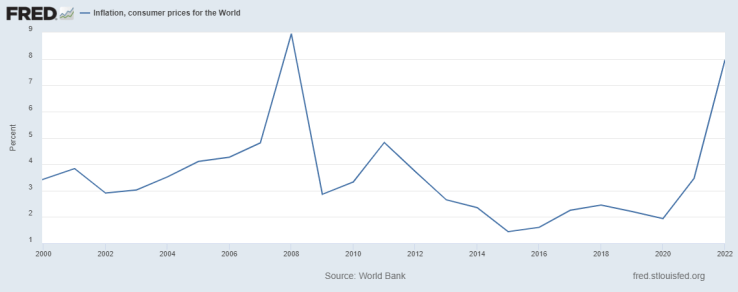

Returning to global economic growth, US and China will have to pick up the slack as global growth engines, even as they continue to be at loggerheads with each other. The IMF has recently issued an update to their World Economic Outlook, revising growth rates slightly upward for many economies and regions on the basis of inflation lowering faster than earlier thought. That doesn’t mean the fight against inflation is over, and we expect our central bank in India, RBI, to announce its latest policy today. If you look at the charts above, the first chart from the US Fred website shows the trajectory of consumer price inflation across the world between 2000 and 2022, while the second chart from the IMF data mapper section of their website indicates the trajectory of inflation across different regions of the world and how they will trend down after 2024. I selected these regions because they seem prone to high inflation and you can see the exact levels of CPI for 2024 in these selected regions here (do scroll down to the chart on this IMF page).

Global trade too seems to have picked up in Q4 2023, from what the WTO Chief said at Davos in the concluding discussion, though concerns persist over the Red Sea attacks and costs of trade rising due to longer shipping routes.

Finally, we need to watch out for the three ‘I’s even though there aren’t any in the global economy. Inflation, interest rates and AI investments. These will keep businesses and governments occupied through most of 2024.