Just three years ago, at the start of the Covid-19 pandemic, many including The Economist were writing about governments getting bigger. Governments did indeed get bigger, as it was their responsibility to control the pandemic and provide relief to vulnerable families across the world.

While the kinds of relief and stimulus packages differed from country to country, depending on their capacity to fund these programmes, let us not forget that governments had to step in and also pick up the slack in investment, so that economies could continue to grow even while in the grip of a pandemic. This took the form of infrastructure investment in India, as I am certain it did in many other developing countries as well. It was argued at the time that infrastructure projects have a multiplier effect and would help build capacity, as also create jobs. On the latter, I think there is a considerable time lag between an infrastructure project getting announced and it being able to generate employment. In India, thanks to a severe 4-month all-India lockdown imposed in 2020, we saw unemployment soar to the mid-20s, before it finally came down.

Since 2021, when the pandemic waned and lockdowns were being relaxed around the world, we saw a surge in pent-up demand. People wanted to be out wining and dining, shopping, watching movies or the theatre, travelling on a vacation, etc. We saw the result of all that pent-up demand being released, in corporate earnings through 2021 and even 2022. Corporate earnings never looked in better shape, in India and across the world, at least for MNCs. And thanks to all that surge in consumer demand, there were supply shortages that first fueled inflation higher, before consumer demand itself began contributing to it. And while this led to record revenue growth and profits initially, it wasn’t long before commodity and wage inflation caught up and started to eat into margins.

As corporate earnings pour in for the first quarter of 2023, we can see that in certain industries and in certain markets margins are still under pressure, even as revenue growth is good. A few global banks and the energy sector are the biggest gainers as they benefit from interest rate increases and global energy prices and demand. The question is, when will private sector investment pick up? I suppose here again the answer depends on the situation in each country and economic region.

According to the UNCTAD World Investment Report 2022, which actually reports on 2021, private sector investments in the form of FDI recovered to pre-pandemic levels globally in 2021 itself. This recovery according to them was driven by MNC profits, with 75% of it driven by developed economies. Total FDI inflows reached US $ 746 billion. However, there are regional variations as well as in the nature of the investments. Infrastructure project finance deals were up 68% and cross-border mergers and acquisitions by 43%, with greenfield projects up by only 11%. And while the value of greenfield projects was up by 15%, they stayed flat in developing economies.

Similarly, for FDI inflows, they grew by 30% in developing economies, but doubled in the US. On the other hand, outflows from developed economies more than doubled in 2021, due to higher M&A activity and MNCs reinvesting their earnings. Some of this must be viewed with caution, as FDI flows both into and out of the US tend to be high, doubling in each case. The net FDI position is what is important, as are FDI stocks over time. Besides, a lot of FDI these days tends to move though equity markets.

What we ought to be mainly concerned about here, are investments on the ground that create jobs. New greenfield projects as well as brownfield ones that are expansion of capacity. There doesn’t seem to be very heartening news on this front yet. And there isn’t likely to be any for another year or more. Because the world is going through a series of interest rate hikes being imposed by central banks in order to control inflation which, in some countries, had soared to 40-year highs. Most companies are probably taking a wait and watch approach, to see how much consumer demand weakens due to inflation and interest rate increases, before they commit to new investments and expanding capacity.

In India, where I have been writing that consumption demand has been weakening for many years even before the pandemic, business investment has grown to levels higher than the pre-pandemic years. However, I think that the bulk of the gross fixed capital formation that has taken place is still the government’s and not the private sector. And with the government increasing capex in FY24 by 30% over the previous year, they expect to crowd-in private investment. In my opinion, it is not the crowding-in or out that mattered these past three years. In fact, because cost of capital was so low, there was every incentive for companies and the government to invest. But because many Indian companies were still faced with excess capacity from years gone by, they need to know that the rise in consumption demand is not merely a release of temporary pent-up demand, but something more enduring in nature.

That more enduring rise in consumption demand can only come from greater job creation and higher wages. In India, unemployment is still at very high levels, although it has come down significantly in western developed economies. Unfortunately, now we have a situation where consumption demand and investment demand will weaken again because of inflation and interest rate increases. So far, consumer demand in the US has been quite resilient to inflation, but economists expect that it will weaken later in 2023, when there might even be a mild recession in the country. US Q1 2023 GDP has already come in lower than the previous quarter at 1.1%, suggesting a slowing down of the economy. Meanwhile inflation is proving hard to tame, and the US Federal Reserve has once again raised interest rates by 0.25%. The ECB in Europe followed suit as inflation in the Eurozone has again ticked up after cooling down during the previous five months. In India, we have had a recent interest rate increase, but since the previous inflation number came in lower than it has been in many months, the expectations are that the RBI might pause rate increases at the next policy meeting.

What is a bigger driver of investment of the greenfield and brownfield type, interest rates or consumer demand? I believe it is the latter as even if interest rates were benign, if a company is faced with excess capacity there is no reason to invest more. However, a lot of corporate investment crosses borders and companies are always on the lookout for a market environment that is promising in terms of healthy and growing consumer demand, favourable factor conditions, as well as low interest rates. And even though interest rates have been low for the past three years, greenfield investments barely grew.

What has grown, however, are the stock markets. Thanks to all the easy liquidity available these past few years, corporate stocks and profits have soared. This has also led to unprecedentedly high levels of share buybacks by companies. As I wrote earlier, media reported global share buybacks to the tune of US $ 1 trillion in 2022. And it was reported that stock buybacks set off a US $132 billion start to this year, 2023, as well. All this is also boosting corporate profits, remember.

So where are all the profits going? Just sitting in reserves, or being invested in financial assets and other investments of a financial nature? During the post-Financial Crisis recovery years, I remember reading that companies were reporting significantly larger “other income” in their corporate earnings. I tried searching for information online on what percentage of corporate profits global MNCs have in reserves, but couldn’t find any.

It is fair to say at this point that all corporate private sector investments do not have to be in greenfield or brownfield projects. The US, for example, reports business investment, which is not only gross fixed capital formation, but includes investment in technology or business equipment as well as in intellectual property. The latter has been growing considerably in recent years. Related to this is private sector investment in research and development which too has been growing. I don’t think UNCTAD’s report takes all of these into consideration.

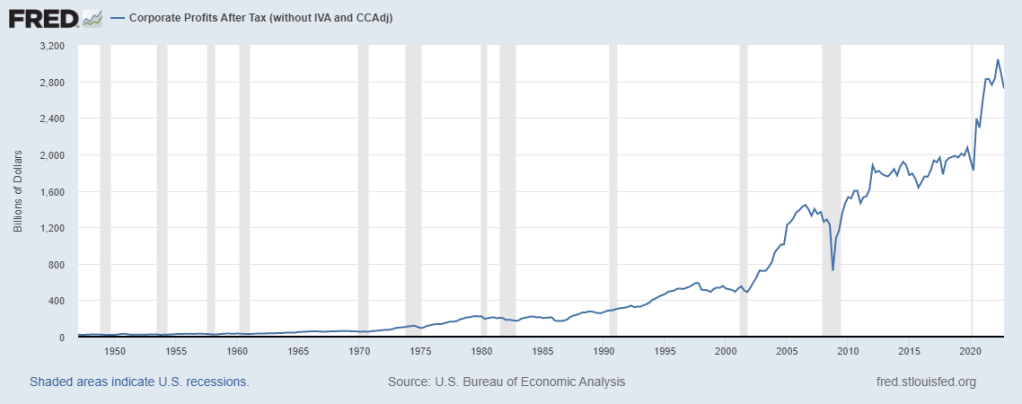

According to the corporate profits data available from the Federal Reserve Bank of St Louis (US FRED), profits reported by US companies saw a drop from the highs of US $3.04 trillion in Q2 of 2022 to US $ 2.72 trillion in the last quarter of 2022. The BEA (Bureau of Economic Analysis) reports that there was a drop in profits sequentially in the last quarter of 2022 of 2%. Barring the last quarter of 2022, there is quarter on quarter growth in US corporate profits, sequentially both in domestic industries as well as in the rest of the world segments. On an annual basis, however, profits grew much slower in 2022 at 6.6%, in comparison with 2021 when they grew 22.6%. And if one looks at business investments in the US during the past couple of years, they do seem to be growing in technology, in intellectual property and in research and development.

Coming back to the subject of private sector investments, greenfield investments are said to be slightly more positive in certain industries such as semiconductors, thanks to the global supply shortage in chips, and in green energy. However, the investments in renewables which are also believed to create more jobs, pale in comparison with those in fossil fuels which still continue to rise, thanks to the global energy crisis brought on by the war in Ukraine. And according to this Global Investment Trends Monitor by UNCTAD, international project finance deals in climate change mitigation weakened in 2022. Overall, they say we can expect a weaker investment climate in 2023 globally.

It wouldn’t be half as bad, if companies at least invested in brownfield investments, in research and development and innovations during this year, and until such time as consumer demand really picks up, rather than increase share buybacks and dividends every other quarter. And after all the boom in business especially in the tech sector during the pandemic years, we are seeing record layoffs this year already. The logic of the markets is perverse in that shareholders cheer job cuts. Instead of complaining that governments are getting bigger and crowding out investment, it’s time that private sector stepped up to the plate and did its share.

Just the other day when the ECB head, Christine Lagarde, announced an interest rate increase of 0.25%, she also urged eurozone countries to roll back their subsidies to households in a phased manner, as the energy crisis fades. And that energy supply capacities are enhanced to keep prices stable. How about energy companies and OPEC members increase their output instead or at least not cut production, so prices stay lower and stable?

It appears then, that we aren’t yet out of the shadows of the pandemic and certainly not out of the Ukraine war impact, either. While governments do their bit, can the private sector prove its mettle, by continuing to innovate, especially in new areas such as green energy and clean technology?