In the fall of 2020, we were relieved to see a recovery in the sales of passenger vehicles in India, as people clearly showed a preference for owning their own private transport in the post-lockdown phase of the Covid-19 pandemic. Companies were reporting better sales as the previous couple of years had seen a slowdown, thanks to a combination of factors, including higher prices on account of compliance with new regulatory norms on emissions, etc., as I had written before on my blog.

That relief has been short-lived, it appears, as several factors have once again come together to slow down the pace of Indian Motown. Supply chain problems, especially to do with chip shortages and the soaring price of fuel in India, along with high prices of most commodities thanks to the Ukraine crisis, are all threatening to put the brakes on India’s automobile industry.

Like much to do with the Indian and the global economy in times like these, this is also a story in two parts. It appears that some automobiles are worse-affected than others; two-wheelers as well as compact and sub-compact cars at the entry level of the industry, are facing a bigger slowdown, as these cater to the most price-sensitive customers. With the result that many automobile companies are stuck between two lanes – trying to speed up production to meet their waitlisted bookings which have piled up due to the semiconductor shortage, while at the same time trying to deal with the slowdown in smaller vehicles.

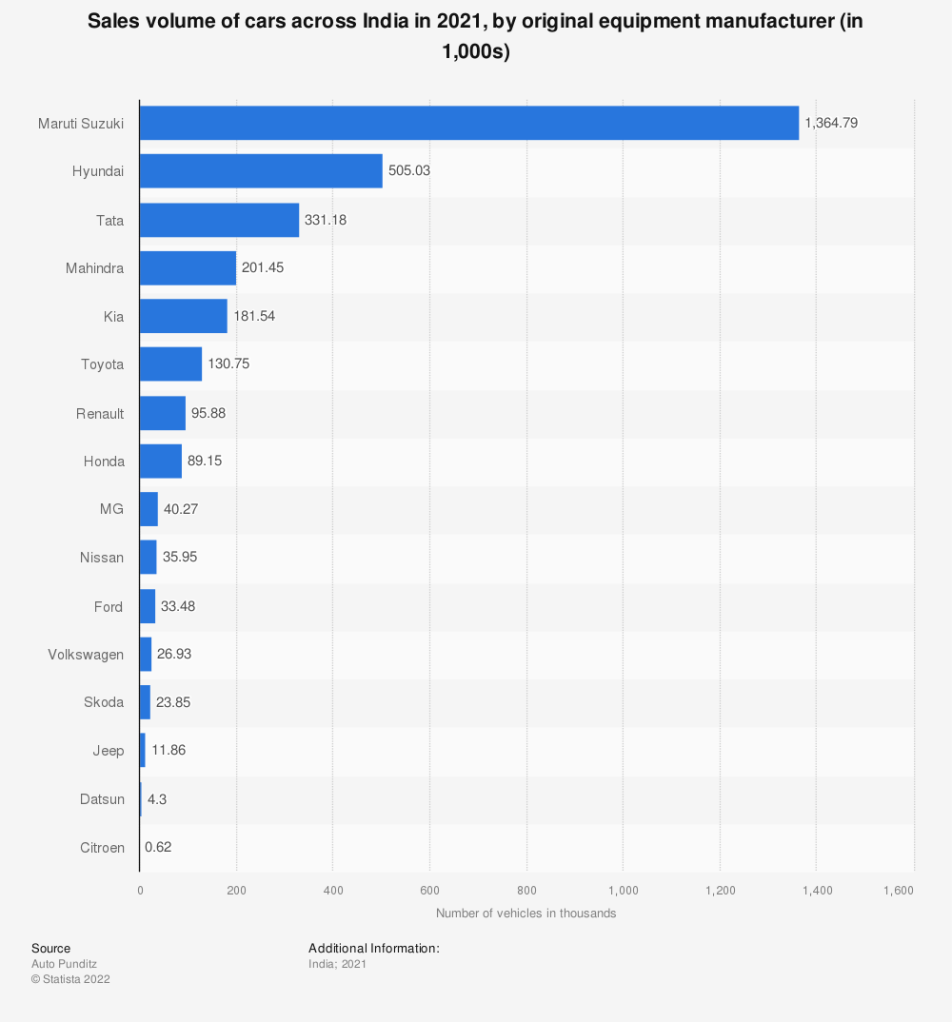

In the latest month for which we have company wholesale figures, we can see that some companies such as Tata Motors have reported a massive 186% increase in sales over the previous year, while others such as Maruti Suzuki have reported much more modest growth, and two-wheeler companies are still seeing slowing growth. Of course, Maruti Suzuki only makes passenger vehicles and within that, they make plenty of the smaller cars. This has surely affected their overall sales, though the company is said to have had better exports this time around. There is also a base effect operating, as last year was a slowdown in domestic sales. Retail sales for the car companies for FY22 have grown 7% over FY21, but challenges remain, according to this article.

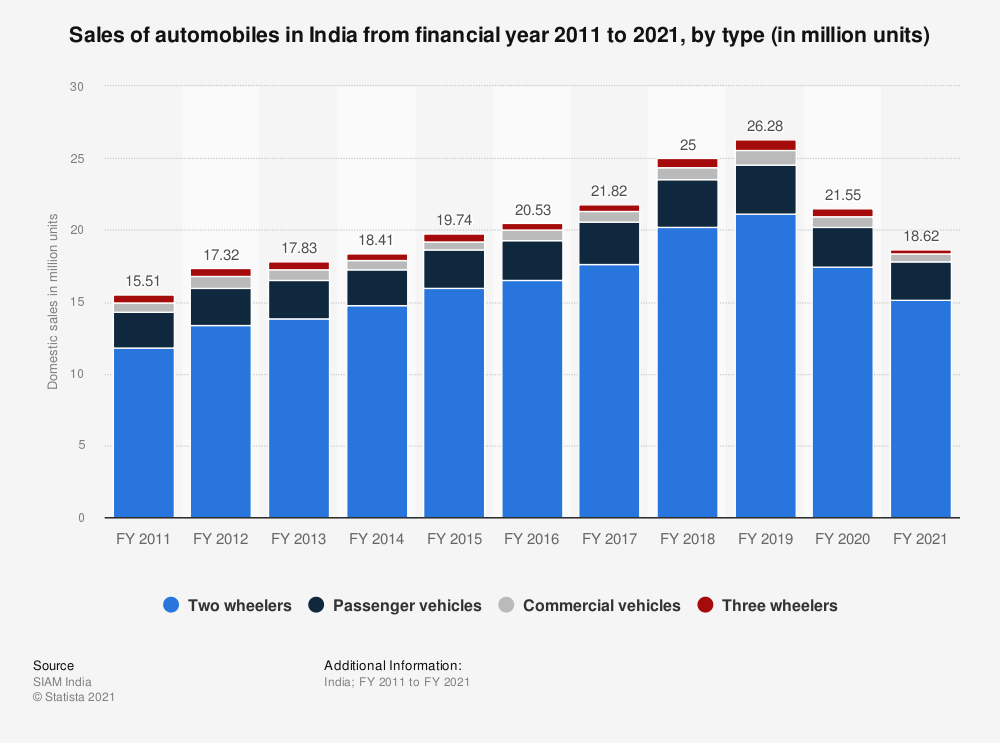

In 2021-22, while passenger vehicles as a whole have grown over the previous year, they are still not back to 2018-19 levels. It’s the same with car registrations, which have grown year on year, but not yet to 2019-20 levels. Meanwhile, according to SIAM (Society of Indian Automobile Manufacturers), passenger car domestic sales have declined, while that for utility vehicles has grown and vans have also grown slightly.

High and raging inflation is definitely affecting demand and sales of most products and services, especially discretionary goods such as passenger vehicles. In fact, the soaring fuel prices are believed to have accelerated the shift to electric vehicles, and Tata Motors have been the biggest beneficiaries of that shift. There are said to be 19,000 Nexon EVs already on Indian roads, which I think is the largest selling electric car to date in the country. In fact, the total number of EVs in India (which includes bus fleets and two-wheelers) is rising quite rapidly, and is currently over 9 lakh vehicles, with UP, Delhi and Karnataka being the highest in EV technology adoption.

I am not sure that is something to cheer as yet in India, because the bulk of the country’s power is generated using coal, not even natural gas, let alone renewables. It is reported that India generates 40% of its power using renewables, but one is not sure how true that is. Unless the shift to electric vehicles forces the government and business to generate more power using cleaner fuel such as natural gas and renewables – an event which is highly unlikely, post facto – this could have disastrous consequences for our environment over the medium to long term.

In the premium mid-size and large cars segment, it has been sports utility vehicles taking over, for the past decade and more. Not that many Indians drive out of the city all that much, or do off-roading trips, but SUVs have presence and might on Indian roads and they can muscle out others in their way. Besides, they are much larger and can accommodate large Indian families. In fact, one brand that helped popularize the SUV in India more than even the home-grown SUV favourites such as Tata Safari and Mahindra Scorpio was Renault. Its Duster model was a huge hit in India, since it was very competitively priced. The past decade, of course, has seen SUVs get smaller and compact SUVs are the rage these days. These and (7-seater MPVs) such as Toyota Innova and Honda WRV have gained traction as well, albeit in a higher price segment.

The growth of SUVs and other larger cars doesn’t seem to face any problem at the moment and these are growing well. Luxury cars are doing even better, which suggests that cars for the affluent and well-off are safe and guaranteed growth for now. Surprisingly, the shift to electric vehicles hasn’t taken place in these premium and luxury segments, where one would have expected a greater concern for the environment and less resistance to price.

The biggest problem seems to be with entry level cars and small hatchbacks. If this trend continues for a longer while, companies will be faced with a difficult choice: to either exit the segment altogether (a tough one since it is the bread-and-butter segment for some of the large car companies) or to innovate much more. Innovation comes with its own costs, but the entry level hatchback segment also provides large volumes and so economies of scale do exist. Unless, the entry level car segment itself implodes, with customers either preferring to use ride-hailing as was the case before the pandemic, or using the metro since many Indian towns and cities are now developing the urban mass rapid transit system.

In India, though, the metro rail was meant to ease the burden of bus and autorickshaw transport from crowded and congested Indian roads. And unlike in the West, most car-owning households have serious hang-ups about using the metro rail in India. There is a strong case to be made for a government campaign to promote metro usage in Indian cities, which tackles the prestige issue head-on and makes using the urban metro rail a sensible and intelligent thing to do.

In terms of innovation for the entry level car segment, I thought a few possibilities could be considered. First, is the use of new, less expensive materials and innovative car design. I am not sure how much less expensive it might be to use more aluminum (which is also recyclable) and carbon composite/fibre glass. In terms of design, perhaps more research is first needed to understand who the entry level car buyer/driver is these days. If it is a college-kid or a youngster just starting work, perhaps smaller, more compact designs might help, with the right brand positioning. Imagine a two-door coupé with a sporty design and the right kind of communication to go with it. If nothing, the sheer novelty of it would attract customers and might help to revive interest in the segment all over again.

Second, the possibility of reviving Tata Nano as a souped-up entry-level car to address this particular segment. It died because it had shortcomings as a product (no glove box, no side-mirrors, etc), but more importantly, because it had the wrong brand strategy. The car should never have been positioned as the cheapest car, nor should it have had a price hanging over its head. That said, it was a well-designed car and probably needed to be positioned right. It could have gone on to be the “Beetle” of our times. If Tata Nano could be redesigned as an electric car with a CNG variant, it might be even better.

Third, offering car rentals to entry level car buyers might resonate with the customer at this time. It might also be a good way to test the market for mobility as a service in the future, where I think the world is headed. As I have mentioned before on my blog, JLR is said to be running a subscription-based mobility plan in the UK, according to their corporate website.

Here again, the brand strategy and communication have to be spot on, in terms of making it available as a service, that is backed by a reputed car company brand and that is backed by technology of today and tomorrow. The important thing to note here is that any comparison with owning a car must be avoided, and to that extent, even calling it a car rental is best avoided. It must be presented as a tech-backed service in its own right that is available on monthly, half-yearly and annual plans.

All this, only if the Indian car industry is at an inflection point which, I think it might well be. Meanwhile, carmakers need to study the used-car market as well and see if consumer demand there is strong.

In the premium and luxury car segments, companies need to focus on creating meaningful product upgrades and by that, I mean those that go beyond cosmetic improvements. Besides, I think it’s high time that car companies invested in building their brands, not their car models or sub-brands. I have observed that Indian automobile companies think that launching a plethora of new ‘brands’ every year is the answer to slowing sales. No, building your main brand and introducing sub-brands thoughtfully in the relevant car segments are what will attract customers. New generations of sub-brands too have to be next-generation in the real sense of the word – upgrade in technology, engine power, transmission type, navigation system, etc. And sub-brands need to be built in such a way that they are in sync with the main brand, and keep adding value to it over time, thereby creating preference for the main car brand.

Luxury cars are on a growth path, even in a poor, developing country such as ours. It is another matter that our government keeps import duties on parts and components so high that they end up being frightfully expensive. Then we have the highest GST rates on them, so the government ends up making even more money from luxury car sales. On the other hand, the high import duties are meant to force these luxury carmakers to indigenise their production as much as possible, but I doubt that is happening on any significant scale. As long as there are wealthy people willing to spend a fortune on a luxury car – including wealthy farmers in villages and those getting rich overnight on land sales in rural India, I might add – both manufacturers and the government are happy.

On that note, I shall put my mind to work on a luxury car brand next! Having worked on brand strategies for JLR corporate, Jaguar and Land Rover as well as brand campaigns for all of them which I have shared on my blog already, I thought it might be a good idea to attempt strategy and ideas for Porsche. The brand that I think is Jaguar’s true competitor, one that Jaguar should pit itself against.

I do hope the inflation situation in India eases soon, though right now that seems like wishful thinking. And that Indian auto companies prepare themselves for some tough times ahead, with product innovation especially at the lower end of the market, planning sensible product portfolios and investing in proper brand building and communication.

The featured image at the start of this post is of a traffic jam in Delhi by NOMAD, CC by SA 2.0 on Wikimedia Commons