As we come to the end of the second pandemic year, we are being forced to confront the same old ugly reality: rising inequality. Come to think of it, we have had to live with this for the past couple of decades and more. And despite two massive crises of a global nature – the 2007/8 financial crisis followed by the Covid-19 pandemic – as well as governments’ best efforts, we are nowhere near solving the problem. In fact, the two global crises might have exacerbated the problem, with easy money, too much liquidity for the wealthy to invest in assets, but not in job-creating businesses on the one hand, and small businesses struggling to stay open and retain jobs on the other.

How did it get this way? Well, if you ask populist, right-wing political leaders they’ll tell you it’s globalization and all those jobs of ours going elsewhere. It’s also immigration they’ll say, and all those people coming here and taking away our jobs. When it is the political leaders who have simply failed to anticipate and recognize the problem correctly and early enough to check it with sensible policies.

There is no doubt that globalization was a major force in shaping the new world order of business, trade and investment in the past half-century. Large, multinational companies, including large financial services companies and banks, led the charge in opening up new markets across the world, with the promise of improving our lives and work, through greater investment. Governments of both origin and destination countries were only too happy to allow freer access to their markets, if it would help their economies clock faster rates of growth and bring better and more jobs. Multinational companies were either looking for low-cost manufacturing centres, or for larger, more lucrative markets, or both, as was the case with China.

Plenty of investment and jobs flowed into developing and emerging economies, especially since 1995, with varied patterns and degrees of success. According to the World Bank, net FDI inflows for the world touched a high of US $3.134 trillion in 2007, and even after the sharp fall due to the 2007-08 financial crisis, managed to reach US $ 2.745 trillion in 2016. The fall in net FDI inflows between 2016 and 2018, when it hit a low of US $ 1.068 trillion, was probably due to Trump’s trade war, which would have influenced global investment flows as well. What’s more, if you see FDI net inflows as a percentage of GDP, that too shows a similar pattern, with smaller developing and emerging economies gaining.

Overseas investment that went to countries in Africa and Latin America were mostly in commodity-led businesses like agriculture, trading, and mining. We do have the exception of Mexico, though, that benefitted hugely from the NAFTA pact between it, US and Canada. The bulk of manufacturing type of investment went to emerging economies in Asia, particularly in South-east and East Asia, which already had a strong base in manufacturing. Today, most of these countries are part of global supply chains, supplying everything from semiconductors to electronics components to machinery and equipment. For most of these countries, globalization has been a force for good, bringing thousands of new jobs, creating new opportunities and lifting people out of poverty.

In India, we have the strange situation of being a big FDI destination, but without the benefits of those investments actually reaching the poor and the middle classes. That’s because most of the foreign investment that flows here is in our capital markets and not in job-creating, on-the-ground investments. And most of the private equity investment from overseas is in our property and real estate sector. We have to wonder if it’s because our workforce doesn’t have the requisite skills, or if our market is not large or lucrative enough for multinational companies to operate here, but that’s a separate discussion.

While these investments and jobs have been flowing to developing and emerging economies – mostly on account of labour cost arbitrage – developed and advanced nations have been experiencing loss of job opportunities, but equally importantly, an erosion in the education, training and skill sets required for jobs in new industries. These are people in small industrial towns, working in low-to-mid-tech manufacturing, with no college education and no means to acquire new skills. They exist across the US, UK and Europe, with the problem being more acutely felt in the US and UK because Europe still has mechanisms to protect jobs and retrain their workforce.

This brings us to the second force that is shaping our lives and our world in even more dramatic ways. Technology. It has played an equal part in globalisation and in loss of jobs in the developed world, though politicians find globalization and immigration better whipping boys. Much harder to apply their minds to regulating the tech industry, you see. And how can they possibly regulate tech, when they are so dependent on the tech giants for their survival, including for “national security reasons” and for strengthening their “military-industrial complexes”.

On both counts, it is our politicians who have failed us. In developed countries, they failed to prepare their populations for when jobs would disappear and when they would have to provide them with retraining to upgrade their skills or acquire new ones. In developing countries, they failed in ensuring that the foreign investments were used to build and create new capacity, which can happen only when the benefits reach more people and equitably. They have failed to regulate tech, which governs every aspect of our lives and even more so, after the pandemic.

Instead, politicians have jumped at the problem that globalization and technology have created in western economies, seeing it as an opportunity to strengthen their political base. Whether it is Trump in the US, or Brexiteers in UK, Victor Orban in Hungary or the PiS (Law and Justice Party) in Poland, they have cried hoarse about the evils and ills of globalization and all that the elites represent, and spread xenophobic nonsense against immigration. And while there has been a lot of talk about decoupling and reversing globalization, I doubt if it will ever happen in the near future. If there is deglobalisation, it will only be because of political leaders and their short-term electoral gains.

Technology too is on a steady march forward, and its pace has only quickened with the emergence of AI. While technology has the ability to improve and enrich our lives, we mustn’t forget it can also deepen the divides between those who have access to it, and those who don’t. And in the days of the pandemic, when companies had to alter their way of doing business, adoption of digitization is said to have increased by leaps and bounds. This seems to have even forced many small businesses in India to shut down, as I mentioned in my recent blog post on the Indian economy, though we perhaps need stronger evidence of this taking place more widely.

What’s more, even looking at where the world is headed, it is not hard to see that there is a perceptible shift towards services, a lot of it enabled by the internet and by technology. Manufacturing too is getting more sophisticated with cleaner technology as well as digitization, as in the case of 3-D printing. Automation will continue apace, and with the inclusion of AI, we can expect manufacturing to focus on fewer, highly skilled, hi-tech labour in the future. Productivity might finally improve somewhat, which America has not seen since the mid-to-late 1990s, according to studies by David Autor and his colleagues at MIT, which I had mentioned in an article long ago.

In the same piece, I had also written about the McKinsey report on the Future of Work and which sectors are most at risk of jobs being replaced by automation and AI. If I recall correctly, they said transportation was most at risk, followed by logistics, retail and warehousing. And only a few days ago, I happened to read a CNBC article about autonomous trucks being used by e-commerce and retail giants in the US.

If an increasing amount of economic activity is based on getting products and services across to us, and if much of that is automated, imagine what it does to jobs, education and skills requirements. Think of what it will also do to wages and livelihoods. Already the gig economy is creating huge problems of its own in the US, with some people cheering its rise thanks to moonlighting opportunities, while others lamenting the lack of regular work, wages and annual benefits, as also a career path forward. If in the past, manufacturing was the source of good, well-paying and secure jobs, while most of services – except high-skill service industries – was considered low-wage, low skill work, that might not always be the case. In both industries, it now appears that level of skill and education will decide wages, while the future of entire industries will remain in flux for several years.

Separately, I have also written about the future of the automobile industry changing and while hybrid, electric, autonomous and hydrogen cars might all exist, mobility itself will become a service. It already has with ride-hailing, and along with other innovative forms of vehicle-ownership or subscription, private transport will soon begin to resemble air travel.

If this is what awaits the world’s 90%, let us look at how the top 10% or the even more rarefied 1% will work and live. If the two crises have told us anything definitive, it is that the 10% have gotten even richer thanks to easy liquidity pumped in by central banks around the world, most of which has found its way into several asset classes, from stocks to bonds, gold and property. Cryptocurrency, the latest craze and bugbear, too has soared and fallen. In just the first year of the pandemic, the world added 5.7 million more millionaires, and their combined wealth was US $ 418.3 trillion.

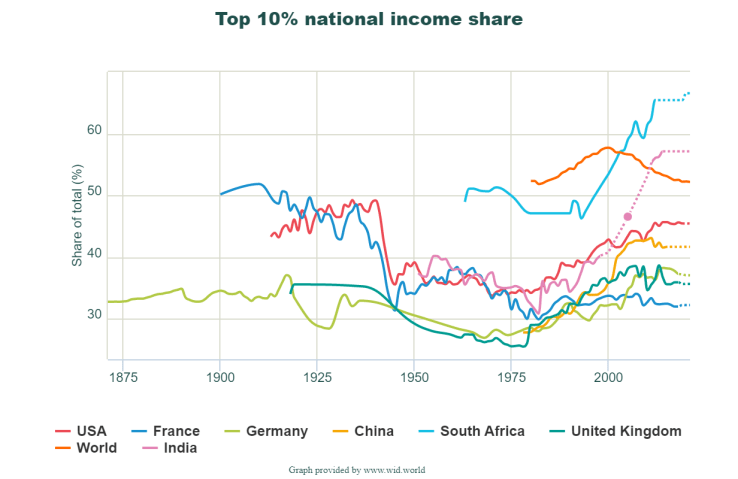

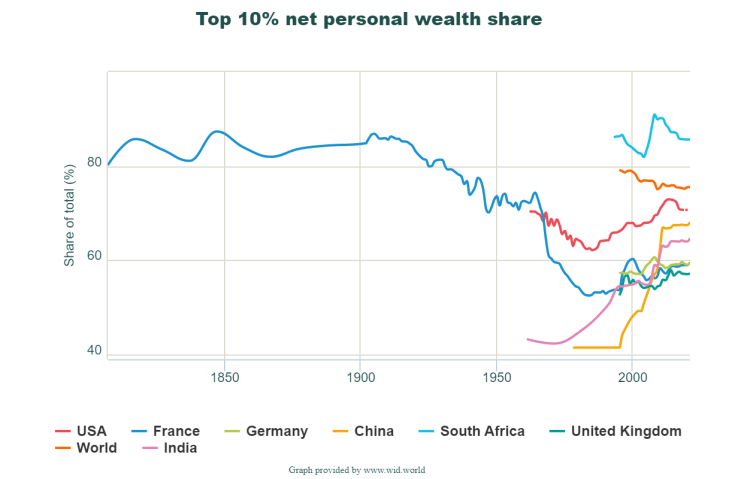

You can see the steady rise of the top 10% in both their share of national income and wealth across the world’s leading and most unequal economies in the charts above, from World Inequality Database. The rise of the 10% also has to do with the way large corporations remunerate their senior management, with their compensation linked to performance and stock markets. And the way they reward their shareholders, through share buybacks rather than reinvesting in their business and helping it grow.

Governments and businesses will have to navigate their way out of this kind of lopsided economic growth and correct the imbalance. Businesses will have an easier time of it, having already received generous tax breaks in most major economies and generated record profits, as well as pared their debt levels to manageable levels. That is not to say that there won’t be additional and legitimate demands made of companies, especially in terms of generating good quality jobs, providing the necessary upgrading of skills and wages, etc.

The onus on governments, though, is greater. To start with, their debt levels have soared through trying to control both the global crises and they will have to start raising taxes to pay for at least some of their debt. Even in ordinary circumstances, the way for governments to check the rise of inequality (both of income and wealth) is to raise taxes on the wealthy progressively as well as pursue redistribution of income towards the poor and needy masses. These are tried and tested methods, but what is needed is the political will to implement them. Already, Biden’s big spending infrastructure plan in the US has run into stiff opposition, and it looks as though higher taxes on corporates and the wealthy is not likely to go through. This, after having spent most of his term trying to negotiate a bipartisan agreement. In the UK, it looks as though higher taxes might be implemented, though we will have to wait and see what form they take.

I have been arguing for higher taxes on corporates and the wealthy in India for the past couple of years, especially on account of Covid-19, but the government prefers to please the elites, while burdening the common man with higher fuel prices through higher indirect taxes which are known to be regressive and super-inflationary.

However, taxes and redistribution of income alone won’t be adequate in the new world that we are approaching. It will be education, healthcare and skills that will make all the difference to how economies fare. While these were always basic requisites for economic growth, their importance in a globalized, tech-driven world is even more paramount. What’s more, it won’t be enough to merely ensure access to better education at all levels; what is required for countries to stay competitive in the future is continuous and long-term upgradation of education and skill sets and standards.

To aggravate the inequality already prevalent in most countries around the world, we have the added problem caused by the pandemic, when millions are sliding back into poverty. According to the World Bank and IMF the numbers of people living on less than $1.90 a day will rise, as Covid-induced poverty increases, with as much as 50-60% of these new poor residing in South Asia. Globally Covid-induced poverty would have created 119-124 million additional poor in 2020, with the numbers rising to 143-163 million in 2021.

The way inequality has risen across the world, not to mention the current vaccine inequity, it would be surprising if there isn’t a widespread revolt of the 90% in the near term. What is sad is that political leaders can still choose to not take any sensible policy decisions, but simply whip up resentment against the privileged elites as they have done in past decades. Often even riding the wave of illiberal, intolerant and right-wing nationalist sentiments.

As always, populist politicians will find a way to make political capital out of the common man’s suffering and revolt to take them to yet another electoral victory.