The wars in Ukraine and in the Middle-East have raged on for years and there has been plenty of reporting on it. Not so much on their economies and how the countries are coping. At least I haven’t read or heard anything on the news about their economies, except at the start of the second phase of the Ukraine war when Russia attacked it in 2022.

Then, the reporting was more about how the conflict would affect the rest of the world since both Ukraine and Russia are bread baskets to the world, and also provide many of the chemicals, metals and oil and gas to many countries. Wheat as well as sunflower cooking oil prices were a major concern then, as was fertiliser prices in India, since our country imports critical chemicals from Ukraine and Russia for fertilisers.

It’s time to turn our attention to the economies of these warring countries and look at the human costs of war, in terms of lives and livelihoods lost as well as how the survivors of the conflicts are managing their lives. Unfortunately, in times of conflict, economic data too is a big casualty, as it is difficult to collect, compile and analyse economic data. Still, I did whatever relevant reading I could find online and from just the macroeconomic picture, the situation appears rather grim.

Thanks to the Black Sea Grain Deal agreed by Russia and Ukraine, and mediated by Turkey and the UN in the middle of 2022, Ukraine was at least allowed to export wheat and other commodities for about five months at a time until 2023. The latest news that I could find is from Reuters who report that Russia withdrew from the deal in 2023 and that even under the current negotiations between US and Russia on cessation of firing in the Black Sea to allow safe navigation, foodgrain and fertilizer exports are not yet part of the discussion. This is a pity, as it hampers Ukraine’s economic growth even as the country defends itself in the face of Russian aggression.

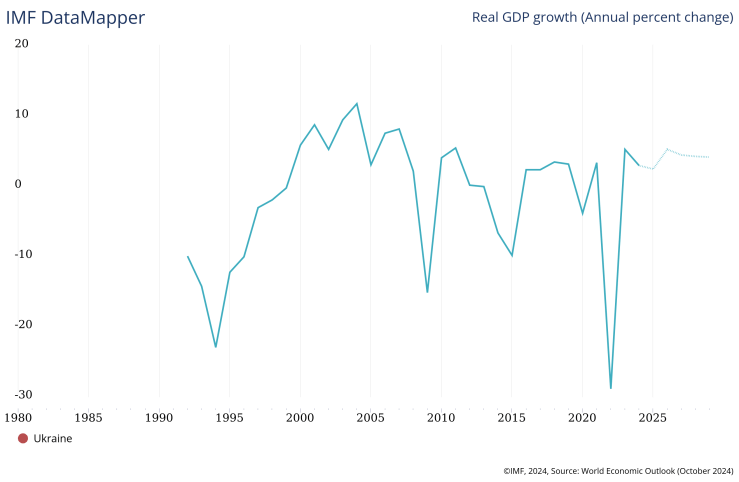

In recent months and through last year, one kept reading and hearing about Russia attacking Ukraine’s energy infrastructure, as well as its cities. I am not aware how much of Ukraine’s industrial capacity is operating, and how agriculture too is faring. From what information I could find on IMF’s website, Ukraine’s real GDP contracted by -28.8% in 2022, while CPI spiked to 20.2%. It is not clear how much of this was brought on by the war and how much was post-Covid impact. In 2023, the country’s GDP turned positive at 5.3% and CPI too trended down at 12.9%. However, growth is slowing more than inflation is, and the IMF forecast for 2025 is GDP growth of 2.4% and CPI of 9%, which is still way too high.

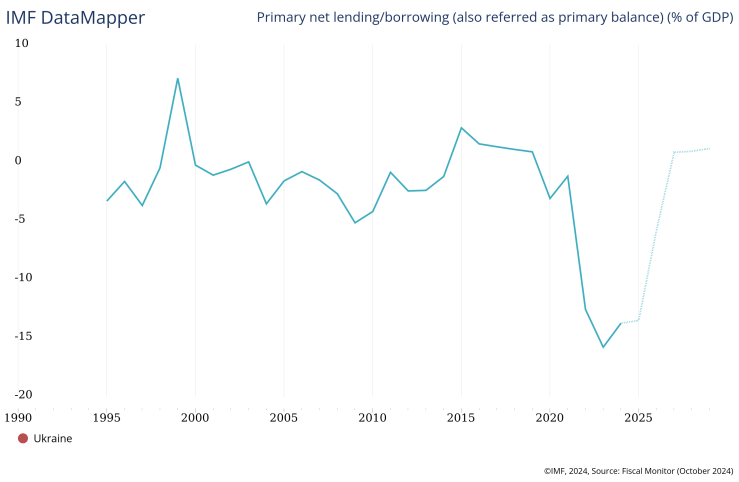

Ukraine is also under huge public debt, with gross general government debt rising and likely to be 106.6% of GDP in 2025. The country has already been under 14 IMF assistance programmes so far. What’s more, Ukraine’s current account which was in surplus of 5% in 2022, went into a deficit of -8.1% in 2024, and is likely to worsen to -14.3% in 2025.

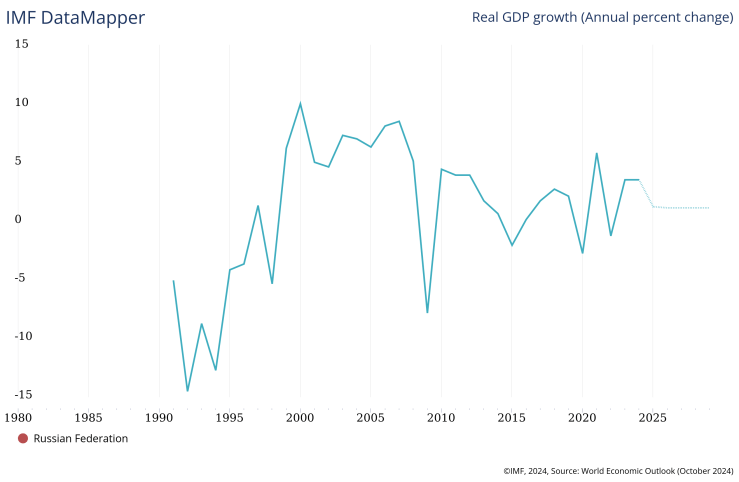

In contrast, Russia’s economy seems to be faring much better. Despite all the western sanctions, the country has been able to export cheaper oil and gas to many countries around the world, India included. It suffered a small contraction of -1.2% in 2022, only to return to positive growth of 3.6% in 2023 and 2024. The IMF forecast for 2025 is 1.4% GDP growth. Consumer price inflation too spiked, though to much less elevated levels than in Ukraine. CPI in Russia has come down to 7.9% in 2024 from 13.7% in 2022, but because Russia continues to churn out defence and wartime goods, because sanctions are still in place, and because of the sharp depreciation of the rouble, shortages of certain goods might be causing the inflation to remain high and stubborn.

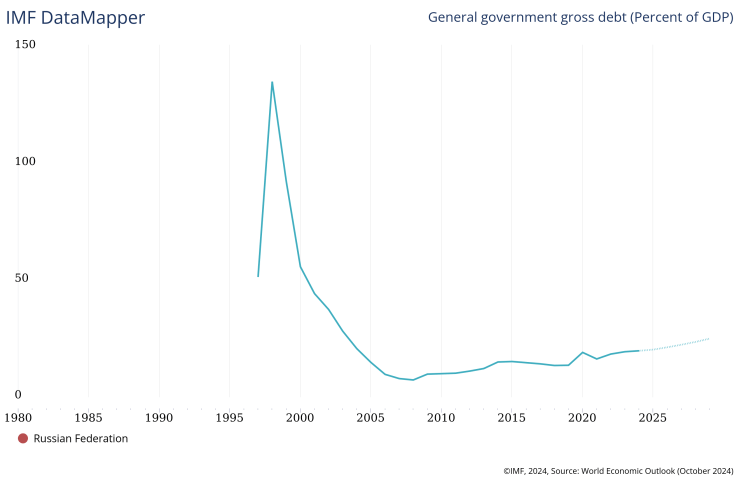

What struck me as odd, is how low government debt in Russia is, and also how small the fiscal deficit. Not just in comparison with Ukraine but in comparing it with other developed economies as well. Normally, such high inflation ought to cause fiscal deficits to rise, but this doesn’t seem to be the case here. With government debt between 16-20% of GDP and fiscal deficit of only -1.67% in 2024 which is likely to fall further to just 0.25% of GDP, we might think Russia is in an enviable position here. It is true that Russia’s current account is still in surplus, but even this has fallen sharply from a high of 10.5% of GDP in 2022, to 2.7% in 2024 and is likely to reduce further to 2.6% of GDP in 2025.

Of course, it’s entirely possible that Russia’s public spending – and social spending as a subset of that – is low in comparison with other countries. On the other hand, private debt seems to be quite high; according to the IMF, private debt in 2020 in Russia was 214.07% of GDP. An analysis by the Centre for Eastern Studies, based in Poland, of the latest Russian budget for 2025 suggests that with Putin directing more of the spending towards defence and internal security, social infrastructure spending will take a substantial hit this year and is likely to leave a lasting impact. Because a great part of the increased government spending on defence was frontloaded to the first quarter of 2025. Reuters reports that Russia’s fiscal deficit increased 14-fold in January of this year, to 0.8% of GDP.

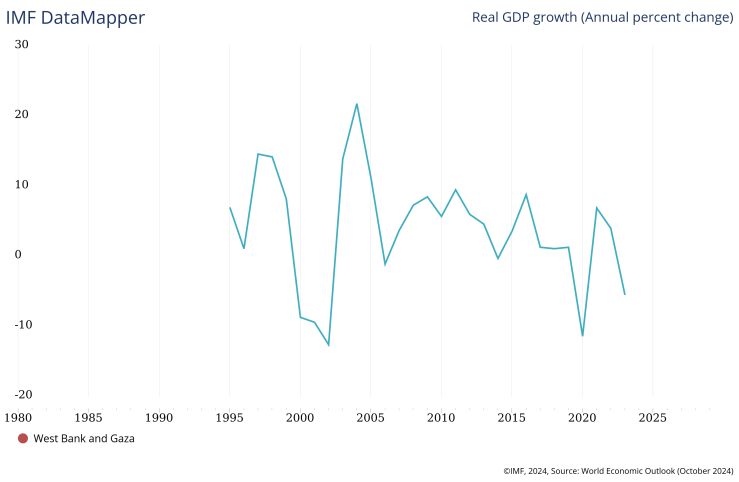

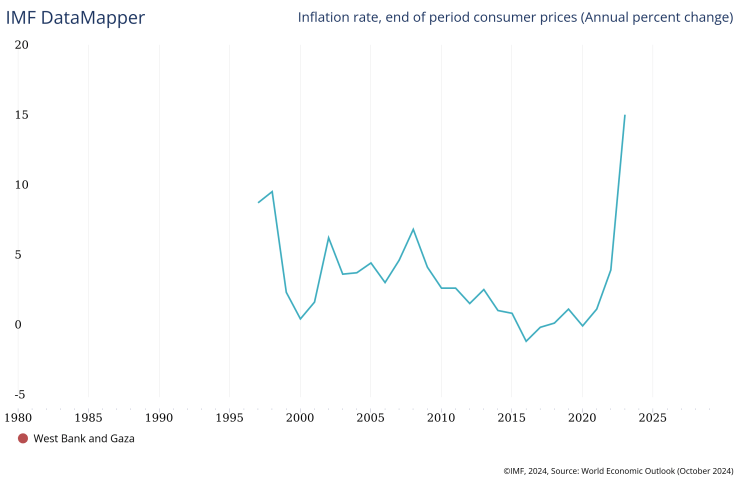

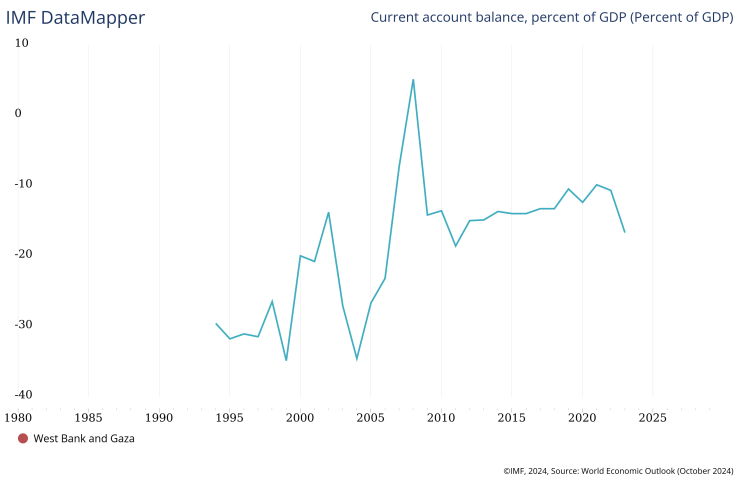

Shifting to the Middle-East conflict, it’s even harder to assess the economic situation. For one thing, data is hardly available for most of the macroeconomic indicators. And here, it appears that much of the economic indicators are perhaps more linked to the post-Covid impact, than the war itself, especially in the case of Israel. The Israel-Hamas conflict has been raging for over a year, since October 2023. I was surprised to find some economic data on IMF’s website for West Bank and Gaza, even if they are clubbed together. Here, GDP was in contraction in 2020 to the tune of -11.3%, returning to positive territory in 2021 and 2022, at 7% and 4.1%, but then contracting again by -5.4% in 2023. CPI, on the other hand, was only 0.1% in 2020, growing to 4.1% in 2022 and 15.2% in 2023! Large current account deficits of -12.3% in 2020 improved to -9.8% in 2021 before worsening again to -16.6% in 2023. While the IMF has no economic figures yet for West Bank and Gaza for 2024, the World Bank Group has a report on the extent of the damage in Gaza and West Bank and its economic cost, which estimates that Gaza’s economy shrank by 83% in 2024, while the West Bank economy also shrank by a smaller 16% last year. What’s even worse is that prices are up by 300% in just one year, and food prices alone have risen by 450% in Gaza.

The sheer scale and intensity of the war between Israel and Gaza has left complete devastation in its wake, with many even calling it genocide or ethnic cleansing at the very least. We know that much of the Palestinian economy, especially Gaza, is blockaded economically, and this UNCTAD press release dated October 2023 highlights the severity of its impact on the economy of West Bank and Gaza. We also know that for decades, the economy of the West Bank under the Palestinian Authority has been dependent on western donor aid although when I searched for the current figure for western donor aid to the region which might have dropped, it was in vain. Al Jazeera reports that several western nations cut their bilateral aid programmes to Gaza and West Bank at the start of the current conflict. What I mean to say is that the Palestinians were already surviving by the mercy of foreign powers for decades, while Israel continued to increase its control of occupied territory. Gaza and West Bank were already weak and emaciated economically, and what chance do they have of survival against this kind of unrelenting Israeli aggression.

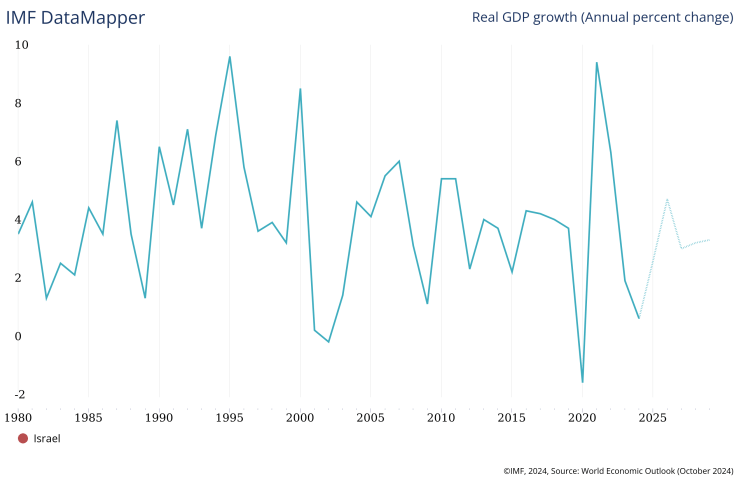

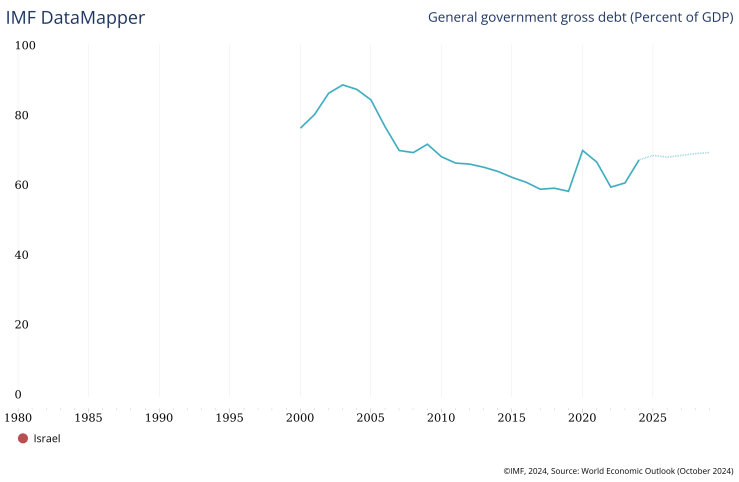

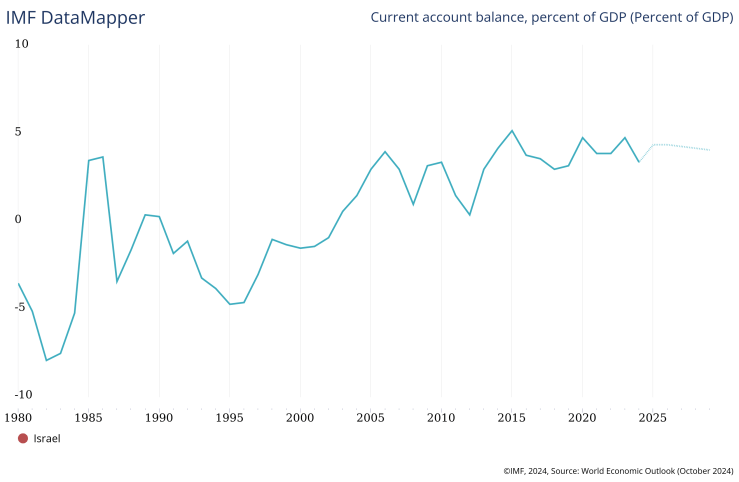

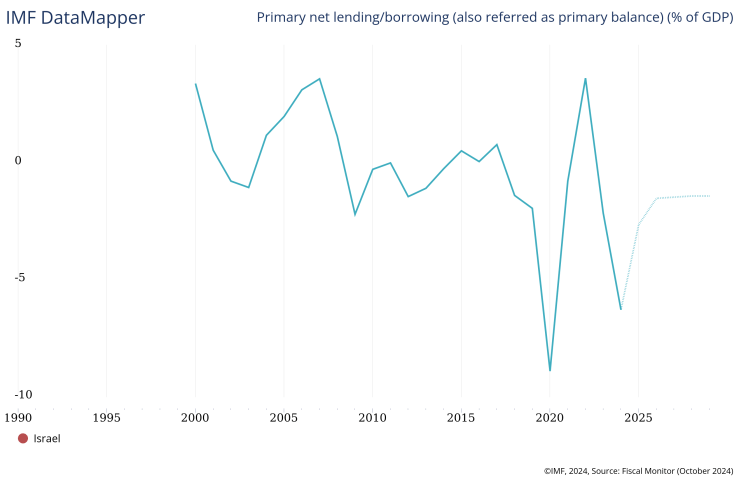

As you’d expect, Israel’s economy is in much better shape. It experienced a sharp post-Covid recovery of 9.5% GDP growth in 2021, that was followed by an equally sharp slowdown from 6.4% in 2022 to 0.7% growth in 2024. IMF projects Israel’s GDP growth in 2025 to be 2.7%. CPI too is in line with international trends – it rose to a high of 5.3% in 2022 before slowing to 3.4% in 2024 and is expected to fall to 2.6% in 2025. Israel’s current account is in surplus right through, and is expected to rise in 2025 to 4.4% of GDP from 3.4% in 2024. The problem is its fiscal deficit which has taken a battering, going from a surplus of 3.62% in 2022, to a deficit of -2.14% in 2023 and -6.27% in 2024, though I must say that the IMF expects a remarkable improvement this year, with fiscal deficits of -2.63%. I suppose the sharp slowdown in economic growth, coupled with the war effort, are taking a toll on its economy. Gross government debt seems to be at reasonable levels, going up to 69.3% in 2025, though private debt seems to be high, at 153% of GDP.

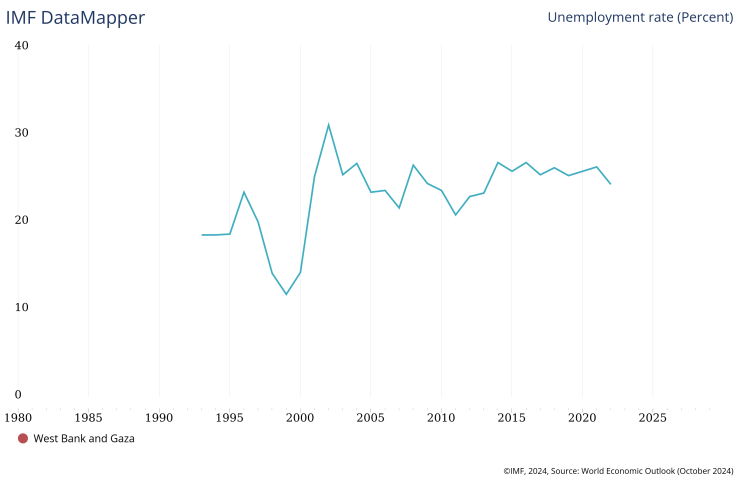

Poverty and unemployment are rife in Gaza and the West Bank as the UNCTAD release highlights. Women and youth are the worst affected, and according to the World Bank both unemployment and poverty are much worse in Gaza than in the West Bank. This latest report from the World Bank highlights the economic impact of the conflict on various sections of the Gaza and West Bank economy.

None of these economic statistics capture the extent of the damage and devastation caused by both wars on their own economies and the rest of the world. More importantly, they don’t capture the human suffering, the lives and livelihoods lost and the deep scars the conflicts will leave on future generations. We can see that the aggressor economies are in better shape than the victims’ in both wars, though the former are not unaffected by the conflict. The longer these wars drag on, the more lives lost, and the greater the cutback to government spending on essential social programs and infrastructure, mean that the aggressor economies too will be weakened over time. Lack of adequate economic opportunities, investment and growth will result in a hollowing out of even the stronger economies, while the plight of the smaller and weaker economies will be unimaginable.

It is time the international community acted decisively and swiftly to end both wars and find a path to sustainable peace. Enough of temporary ceasefires which, as we have seen, take nothing to be broken. Long-term political solutions need to be found, else the wars will continue to rage.

Note: The IMF estimates from their data mapper are from their October 2024 World Economic Outlook and the latest updates are expected later this month at the Spring Meetings. Some of the economic data were also altered on their website within a couple of days of my making a note of them.