It’s around three and a half years since Britons voted in a referendum to leave the European Union by a narrow margin of 52 to 48. That alone should have told UK’s lawmakers how divided opinion is on the issue of whether to leave the 40-year old union with the European Union. After all these years, Britain is even farther away from a resolution than it was in June 2016. Through all the political turmoil, dithering and indecision on what type of Brexit to go for, the main sticking point of the Irish backstop which today’s political dispensation finds unpalatable, the parliamentary debates, Britain finds itself in the worst position ever in recent history.

What’s worse, the nation is even more divided than it was in 2016, with both remainers and leavers hardening their stance and digging their heels in. This has no doubt been the handiwork of politicians who have stoked discontent and fanned the fires of anti-EU and anti-immigrant sentiment to suit their divisive ideologies. With just 45 days to go, the UK government released its Operation Yellowhammer document, a contingency or worst-case scenario report for a No-Deal Brexit. It asks Britons to be prepared for food and medicine shortages, civil unrest and even rioting among other disruptions that could take place in the aftermath of Brexit. Whether the endangered English bird (attributed to EU agricultural policies) becomes a metaphor for Britain’s perilous future is for the Britons to decide.

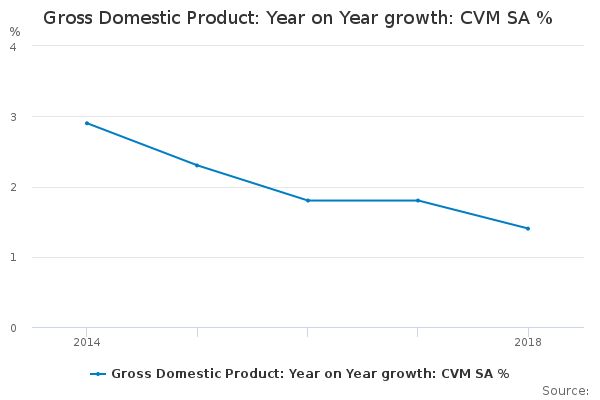

I had written in a previous post that the best way to decide on Brexit and its type would be through elections, but not in the manner being planned currently. I hadn’t foreseen the chaos that would follow Theresa May’s exit, with Parliament being suspended by Boris Johnson, and a No-Deal Brexit as well as early elections being forced on the people. As it turned out, Britain’s Supreme Court ruled that proroguing Parliament was unlawful and so the MPs are back in Commons, arguing and debating, with not much success. In the meantime, Britons have had to go about their work and earn a living. So, it is worth examining what Britain’s fractious politics has done to business and what impact it is having on the economy. It is a fact that UK is still recovering from the 2008 financial crisis and the economy has been slowing considerably since 2015-16. Britain’s GDP contracted in Q2 by 0.2% after slowing to 1.2% in Q1 of 2019. For the entire year, the country’s GDP growth is forecast to be 1.3%.

British banks are not in great shape, as their US counterparts are, even if they are faring slightly better than those in Europe. With financial services as the biggest part of their services economy, nothing leaves them in a more vulnerable position than the decision of several global banks to relocate their London operations to Dublin, Paris, Frankfurt and Amsterdam. London’s and The City’s position in global finance stands considerably weakened.

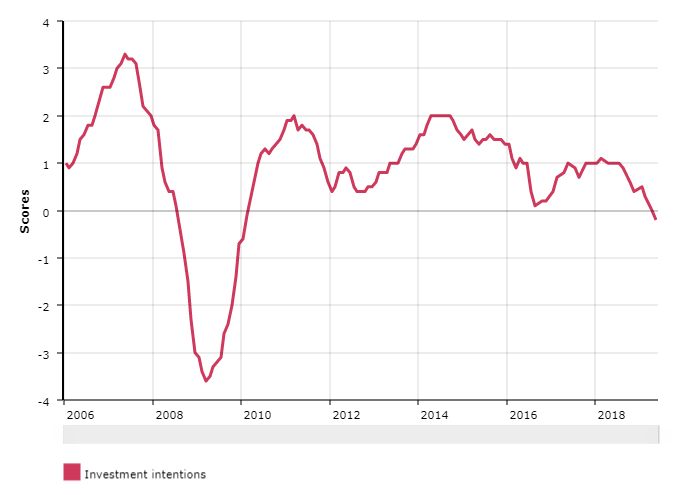

Investment intentions in Britain fell to the lowest levels since January 2010. It is almost entirely attributed to Brexit-related uncertainty and even a short extension of the deadline is not being seen as an opportunity to unlock investment.

Another significant part of British industry is the automobile sector, which has been facing massive headwinds since the Brexit referendum. According to the think-tank, Chatham House, the Japanese warning over a No-Deal Brexit is not an idle threat. Nissan has cancelled production of its X-Trail SUV in Sunderland, putting thousands of jobs at risk. And Honda is stopping production of its cars in the UK by 2021. Britain’s exports to Japan in 2017 constituted 1.6% of its overall exports and Japanese FDI stocks in the UK stood at US $ 152 billion that same year.

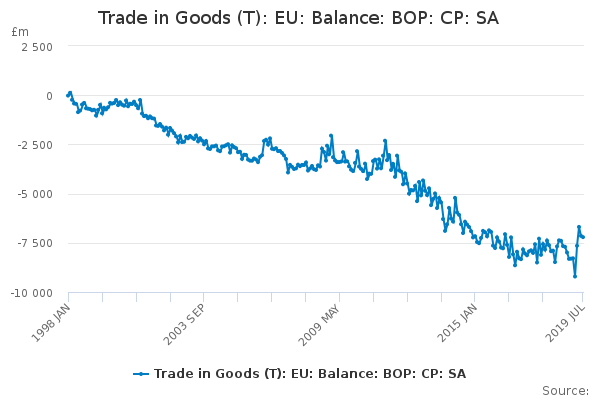

Britain is not just in the throes of Brexit, but is also going to be affected by the ongoing US-China trade war. According to the Office for National Statistics, in the three months to July 2019, UK trade deficit (goods and services) narrowed sharply, thanks to the steep fall in goods imports of around £ 14.1 billion, which includes machinery and that is not a good sign for business investment. In fact, according to a survey conducted by the Bank of England (Agents’ Summary of Business Conditions May 2019), investment intentions in Britain fell to the lowest since January 2010 (see slideshow in article). It is almost entirely attributed to Brexit-related uncertainty and even a short extension of the deadline is not being seen as an opportunity to unlock investment. In other words, UK businesses are not buying their politicians’ arguments of an extension, or kicking the can further down the road, just yet.

CBI (Confederation of British Industry) says 87% of their members cite lack of, or inconsistent, information as a major concern and 41% say that lack of resources has kept them from planning for Brexit.

The Confederation of British Industry, for its part, is doing its best to help UK businesses best prepare and mitigate their losses from a No-Deal Brexit, which has gained currency, ever since Boris Johnson took power recently. In their 128-page document, analyzing the state of readiness for a No-Deal Brexit, they find that there is still considerable ground to cover by UK, EU, UK businesses and the joint negotiating teams: of the 27 areas identified for negotiations and preparation, satisfactory progress has been made by all parties only in 3-5 areas. They urge bureaucrats on both sides to accelerate negotiations and clarify progress made on several factors, all of which affect business. Their website quotes the IMF as predicting that a No-Deal Brexit would lead to UK’s economy taking a hit of 8% in the long-term – an equivalent of £ 6,000 per household. Customs declarations under No-Deal Brexit are likely to cost UK industry £ 20 billion every year.

The document also says that 4 out of 10 SMEs that trade internationally have no contingency plan for Brexit, simply because the funds and access to sound advice required, are unaffordable for them. CBI says 87% of their members cite lack of, or inconsistent, information as a major concern and 41% say that lack of resources has kept them from planning for Brexit.

In a Bank of England Survey, 57% of businesses reported that Brexit was in their top 3 current sources of uncertainty. Within Brexit-related concerns, the biggest sources of uncertainty were customs, followed by consumer demand and supply chain.

In a separate survey done by the Bank of England (Decision Maker Panel Survey Q2 2019) on the importance of Brexit as the source of uncertainty, conducted from February to April this year, they find that 57% of businesses reported that Brexit was in their top 3 current sources of uncertainty – the highest it’s ever been since the survey began in August 2016 – higher than 54% reported in November-January surveys. Within Brexit-related concerns, the biggest sources of uncertainty were identified as customs, followed by consumer demand and supply chain. Further, manufacturers were most likely to have increased stock due to Brexit concerns, followed by wholesale/retail, other production, construction and information and communications industries – ranging from 65% of manufacturers to 25% of information and communications businesses. The survey also mentions the regulatory framework that is bound to change as Britain leaves the EU, which The Economist reported on last year. From the survey, it appears that those businesses which trade more with the EU were more concerned about regulatory changes than others. Chatham House believes that even an orderly No-Deal Brexit (the possibility of that, however remote) will come with huge costs as Britain sets up its own new set of regulations for everything from food and medicine safety standards to automobile regulations, financial services, energy, etc. It will affect vast swathes of UK industry and the cost of conforming to the new regulatory framework will also have to be factored in.

While consumer demand in the UK has so far held up pretty well under the circumstances, it continues to be muted and is clearly a concern with business decision-makers. Shrinking trade and production would at some point sharply affect employment and wages and crimp demand. And just like everywhere else across the world, there is no serious effort at fiscal or structural reforms, only a lowering of interest rates by central banks. Europe is already suffering a sharp slowdown, including in the growth economies of Germany and Netherlands, and the ECB is promising further monetary stimulus in the absence of fiscal stimulus as most economies try and deleverage their mountains of debt.

For the financial year ended March 2019, UK had a gross government debt of 85.2% of GDP and a total debt stock (including households and non-financial corporate) of over 200% of GDP. PwC forecasts the total debt stock in UK to rise to 260% of GDP by 2023, led mostly by households and non-financial companies. That is, of course, if interest rates rise to 2%, which I doubt they will anytime soon, and especially not in the face of Brexit. On the other hand, under a No-Deal Brexit, with businesses cutting back on capex and investments, and trade likely to shrink at least until 2021, the government might be forced to consider a fiscal stimulus. Will it, is the question? Or will they simply turn to the BOE and expect it to cut rates? As it is, the UK government has a £ 30 billion payment due to the EU as divorce bill, which Boris Johnson refuses to pay.

Against this background, the UK risks moving ever closer to the US as it leaves the EU. As I had written in a blog post earlier, I say “risks” because the country is likely to get swamped by the US, especially under the current administration. Of course, with Trump pursuing equally self-destructive policies in the US, who can tell what the next government there will look like? At the moment, however, Boris Johnson’s government is being wooed by the US with the incentive of a juicy free-trade deal, in which everything from automobiles and the NHS are up for negotiations.

Back in the UK, business churn – one of the signs of a healthy business climate – is at its lowest in a long time. For the first time since 2010, UK business births rate dropped from 14.6% in 2016 to 13.1% in 2017 and UK business deaths increased from 10.2% to 12.2% during the same period. In other words, net new business creation fell from 4.4% to 0.9% in the matter of just one year. In such a scenario of shrinking trade and business activity, to hear British politicians talk of “Global Britain” tells one just how out of touch with reality they really are. Michael Gove is recently reported to have said that he believes UK businesses are ready for a No-Deal Brexit, which prompted an immediate reaction from businesses to the contrary.

Boris Johnson has just announced a new Brexit plan, which is being discussed with the EU, but since the main sticking point of the Irish backstop remains unresolved, it seems there is not enough time. And with Mr Johnson still adamant about not wanting an extension and telling the EU that UK is prepared to leave without a deal, there’s no saying how this will end. Besides, the UK parliament has to still agree to his plan and a vote of confidence looms large in the days ahead. Parliament and the EU will most likely force him into an extension.

Businesses, then, can expect more turbulence and uncertainty. Fasten your seat belts, for there could be several air pockets ahead. Or, perhaps Mark Carney’s statement about a “global trade war shipwrecking the global economy” is equally apt for sea-faring Britain crashing out of the EU.

All graphs in the article’s slideshow are from the website of the Office for National Statistics, UK, except for the investment intentions graph which is from Bank of England’s Agents’ Summary on Business Conditions May 2019, featured on the bank’s website.

[…] all countries to start preparing in earnestness for the big divorce. I had written long ago in a blog post about how businesses in the UK are preparing for Brexit, but it looks like they are no closer to […]

LikeLike